Oil prices and energy stocks have suffered of late as the

price of oil softens. Over the past several months we have been taking

positions in the energy space and at current levels are thinking about buying

more.

Supply – Demand Dynamics

The demand side of the equation looks unappealing with the Chinese and U.S. economies under pressure and the threat of global economic stagnation. Saudi Arabia is signaling to OPEC members and the world that it is not reducing production in the face of a perceived slowing of demand and is in fact raising production to meet its forecast of increased demand in 2016. “The world’s biggest oil exporter pumped 10.564 million barrels a day in June, exceeding a previous record set in 1980, according to data the kingdom submitted to the Organization of Petroleum Exporting Countries. The group sees “a more balanced market” in 2016 as demand for its crude strengths and supply elsewhere falters.” (Emphasis added).

The statement shows that the Saudis are expecting the

pricing war in oil to continue into the next year and common sense dictates that

certainly will not be good for oil prices going forward. They expect 2016

global demand of 1.34 million barrels per day, up from 1.28 million this year

and cite strength from emerging markets as the likely source of end demand.

Unfortunately the increased demand thesis is not shared by others

in the industry. According to OilPrice.com,

“The news from the IEA is not good.

“World oil demand growth appears to have peaked in 1Q15 at 1.8 mb/d and will

continue to ease throughout the rest of this year and into next as temporary

support fades.” I don’t have great faith in forecasts but the data shows

declining demand growth from late 2010 to the 2nd quarter of this year (Figure

1). The weak global economy is the cause of low demand growth. The current debt

crisis Greece and collapsing stock markets in China are the latest alarm

signals. Today, the IMF lowered its world economic growth outlook because of

these problems. “We have entered a period of low growth.” —IMF chief economist

Olivier Blanchard. IEA data shows that world liquids production increased 1.1

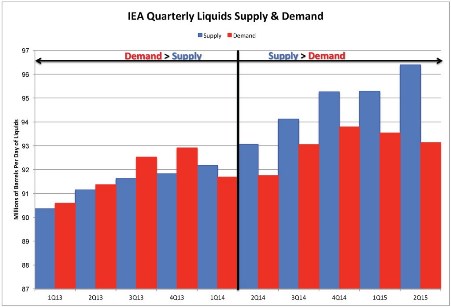

mmbpd compared with the 1st quarter of 2015, and demand fell by 410 kbpd

(Figure 2). Half of the production increase occurred in June 2015. The

production surplus (supply minus demand) that is responsible for low oil prices

continues to increase (Figure 3).”

U.S. inventories also remain a problem. According to recent

data from the EIA (via Business

Insider), “The latest data from the

Energy Information Administration showed a fall in stockpiles by 4.3 million

barrels in the week ending July 10. This brought the total number of barrels to

461.4 million, maintaining them at a level not seen in the last 80 years.”

The supply – demand dynamic appears to have glaring negative

obstacles to overcome but yet there are additional headwinds on the horizon.

Iranian Oil

The Obama Administration has concluded the preliminary

stages on an Iranian agreement that opens the availability of Iranian oil to

the market in return for a nuclear arms deal. The announcement of the deal had

an immediate negative impact to crude prices but oddly enough the price for the

commodity quickly rebounded and ended up rallying from those levels as market

experts digested the data and formulated their own supply – demand dynamics

with the input of new data. Of course

the deal is not completed until it is reviewed and approved by UN Security Council,

the International Atomic Energy Agency and Congress, but for now let’s assume

this deal is primed to go through successfully.

Upon the announcement of the deal, OilPrice.com

stated, “Bijan Namdar Zanganeh, Iran’s

oil minister, said during the OPEC meeting in Vienna on June 5 that his country

will move quickly to restore its status as a major oil exporter once the deal

is signed, beginning with an export increase of 400,000 barrels per day and

adding 600,000 more barrels per day within six months. And just after the deal

with Britain, China, France, Russia, the United States and Germany on July 14,

Zanganeh tweaked that forecast, saying Iran would begin by exporting 500,000

barrels a day, an amount that would grow by an additional 500,000 barrels in

six months.”

According to OilPrice.com,

“The renewed downturn is also sparking pessimism among oil traders. In recent

weeks speculators have taken the most bearish position on oil in years.

Net-long positions on oil – betting that crude prices will rise – dropped by 28

percent for the week ending on July 21. The ratio of long to short positions

for hedge funds dropped to 1.7 to 1, down from 4 to 1 over the past three

months. In fact, net-long positions are at their lowest levels since 2010. In

other words, speculators are the most pessimistic about oil prices than they

have been at any point in the last five years. With hedging positions expiring,

more companies will lose their protection and suffer from low prices. And

unlike earlier this year when banks and equity markets were eager to provide

cash injections into battered shale companies, betting on a rebound, financial

lifelines are not as generous or as accessible as they were just a few months

ago. New loans are coming with onerous interest rates. For some of the weakest

companies, access to credit could soon be cut off entirely.”

So increasing supply and declining demand is bad news for

the energy sector, particularly those companies with exposure to oil price

fluctuations. Indeed every piece of data and analysis on the space reads like

an epitaph for energy companies. So then why have I decided to start building

positions in the energy sector when the entire space is clearly doomed?

For one I am a contrarian investor and believe that there is

long-term value to be garnered from this sector. I also believe that much of

this negativity is already reflected in the price for oil and energy stocks.

It’s not like I woke up one morning and was shocked that there was an Iranian

deal on the table. It has been a political circus for some time. Demand is

declining, supply is ramped up. Again, we know all this. Will oil prices

continue to drift lower? Yes probably. Will prices fall to $30 per barrel as

many are predicting? It certainly could but not for any of the reasons

mentioned above. It will be the unknown that will drive the commodity one way

or the other. No one knows what it will be but it will happen. The best we can

do is invest based on the data that we know and prepare a well planned

investment thesis around the strategy.

What We Do Know

The supply side of the equation shows a glut of oil reverses

and no indication of production slowdowns. That’s not a great sign. We also

know that supply figures have been notoriously manipulated to show an

over-supply scenario. Here is an interesting article I came across in OilPrice.com

that reiterates that point.

“In the past, I

documented the overstatements by both the IEA and EIA in 2014 & 2015 in

terms of supply, inventory and understatements of demand. Others also noticed

these distortions and, whether intentional or not, they exist and they are very

large in dollar terms. These distortions, which are affecting price through

media hype and/or direct/indirect price manipulation, are quite possibly the

largest in financial history. Putting numbers behind it, with worldwide production

running some 95 million barrels per day, and assuming $55 per barrel for oil,

the market for crude oil is about $5.2 billion per day. Each $10/Barrel change

is worth nearly $1 billion/day or $365 Billion/year for the worldwide crude oil

market. Add the worldwide equity market caps of oil and oil related equities

and debt you have a scandal that is in the trillions; a number that cannot be

ignored.”

“According to

Cornerstone Analytics, who have documented the IEA systematically

underestimating demand in 2012-2013 only to revise it higher quarters if not

years later, the EIA has created the appearance of an imbalance of supply by

some 500 million barrels or $2.5 trillion in the last 5 quarters alone. This

has easily swung oil by at least $20/barrel if not more. I have maintained that

oil should have corrected to around $70 in the fall of 2014, tied to U.S.

production increases which at the time represented the price at which drillers

would continue to add to supply. That price tied to cost reductions has

probably been reduced to $60ish currently. But today, with the consensus

oversupply widely quoted in the media as some 2 million barrels per day

worldwide, it’s clear that if the numbers are correct below, the perceived

oversupply wouldn’t exist at all. Suffice it to say prices would be at least at

the point where production would need to be added, perhaps around $60-$70 per

barrel, if not higher. Assuming that number at $70 and with the blended average

of WTI & Brent at $55/Barrel approximately, at $15/Barrel given the 95

million barrels of global production, then we can estimate that global oil

markets are being undervalued by about $1.425 billion per day or over $500

billion per year.”

“Why regulators, and

especially the media, refuse to address this, even in theory, and instead

choose to perpetuate the falsehood of oversupply is beyond me. In the last two

months, E&P equities fell 10 weeks in a row, which hasn’t happened since

1989. To answer our own question on why this entire event is being largely

ignored, maybe that oil is thought to spur higher economic growth as suggested

previously. But so far that has yet to even materialize as U.S. GDP growth has

actually slowed, not accelerated. Only time will tell whether this exaggerated

move in oil, as well as its volatility, is justified or not. As reported here,

the EIA has already revised lower, though only slightly, its prior month’s

production forecast as we predicted. Look for more of this to come.”

We are also well aware of the threat of Iranian oil supplies

entering the market. Once again, the newly struck nuclear arrangement still has

tremendous hurdles to overcome but let’s assume passage of the deal. This does

not mean that Iranian oil supplies will hit the market immediately as Bijan

Namdar Zanganeh suggests.

This Is Why Oil

Markets Shouldn’t Worry About Iran’s Comeback – OilPrice.com:

“So perhaps Zanganeh is jumping the gun a

bit about the speed of Iran’s rebound in the global oil market. One independent

oil analyst, Gary Ross, the executive chairman and head of global oil at the

New York-based Pira Energy Group, said, “It should take a good year between the

day they sign the agreement and when they add 500,000 barrels of production a

day,” he told The New York Times. Yet, Ross concedes that no matter how quickly

– or slowly – Iran restores its export potential, the global market should be

able to absorb it without too much trouble. Today there are about 1 million

more barrels of oil on the market than customers need, but he notes that the

demand has been gradually rising, especially in Asia. As a result, Ross says,

Iran’s goal of eventually adding 1 million barrels per day to the export market

shouldn’t be much of a problem. “With each day, the market will be in a better

position to accommodate the incremental Iranian oil.””

GOLDMAN: The Iran

deal won't impact the oil market until 2016 – Business

Insider: “In a note to clients on

Wednesday, Goldman Sachs analysts predicted that the lifting of sanctions on

Iran will be bearish for oil, though the effects won’t be seen until 2016… A

gradual increase in Iran’s oil exports would start with the drawn down of the

Islamic Republic’s floating storage of c.20-40 mb, once the EU import bans are

lifted. This would be followed by a jump in production, which Goldman says

could lead to a c.200-400 kb/d increase in Iranian exports in 2016. Much

uncertainty still exists regarding the timing of the sanctions relief, and

whether or not Iran will be able to reach pre-sanction production levels, but

Goldman is convinced that the deal will eventually hurt oil prices.”

Gains in Iranian Oil

Output Are Just One Way the Nuclear Deal Will Affect Oil Prices – PIMCO:

“The nuclear accord, of course, is far

from implementation. Among other steps, the U.S. Congress has 60 days to

approve the deal; should it disapprove, Congress may struggle to overcome a

White House veto. The International Atomic Energy Agency (IAEA) also must

verify that Iran has completed its commitments. In short, a lot can still go

wrong. Should all work out, though, over the next 12 months Iran could provide

an additional 500,000 barrels per day (b/d) – a not-immaterial volume but only

one-third of what the U.S. added to global supplies in 2014. Moreover, we view

this increase as more than discounted at current prices…Overall, we view this

as a bearish event, but less because of incremental oil supplies in the next

year and more because of the impact Iran could have on other suppliers over the

long term. In our view, though, much of this Iran risk has been priced in

already.”

OIL EXPERT: 'A

potential return of Iranian oil to the market could not have come at a worse

time' – Business

Insider: “However, it's important to

note that there are still many uncertainties over how quickly Iran will get off

the bench and back into the game. "Restarting of mothballed fields and

reopening the sector to foreign investment faces many obstacles,"

according to Barclays analysts. Additionally, Dr. Mamdouh G. Salameh, an

international oil economist and World Bank consultant, told Gulf News that

Iran's oilfields are old and need huge repairs if the Islamic Republic wants to

increase production. "It will take Iran more than two years to deploy the

enhanced oil recovery (EOR) technology to repair the damaged reservoirs in its

oilfields and try to increase production," he said. "Even then it

might only succeed in limiting the fast depletion in its oilfields rather than

increase production."”

So it’s pretty well publicized that Iranian oil is coming to

market. There are many variables and opinions as it relates not only to the

validity of the Iranian deal but the time it will actually take for the

increased oil production to hit the market full bore. So many variables and

opinions that reflect the worst case scenario in our opinion. Given the

depressed levels of the market and the extreme pessimism surrounding the

industry, any positive news that comes out should have an exponential positive

effect on prices in our opinion.

The Saudi Strategy

The Saudi Strategy calls for lowering the price of oil to

cripple those producers at a higher cost point in order to maintain market

share. The near-term manageable pain felt by the Saudi producers would be well

worth the destruction of the U.S. shale boom and preservation as a leading

producer. This is how I imagine the argument goes. The question arises if the

Saudi’s miscalculated the ingenuity and efficiency of the American capital

machine. It is true that U.S. rig counts have been in a free fall.

That said, U.S. production has not as of yet witnessed a

significant drop in reduction. True many of these drillers need to

maintain production levels in order to meet interest payments on their debt

and keep the operations going. The hope is for survival through a temporary

depression in the underlying commodity. This also forces these companies to

extract higher levels of productivity than in the past and a favorable turn in

the supply – demand dynamic will have an exponential effect on operations and

profitability. If it is found that these companies are unable to withstand the

weakened business climate, there will certainly be bankruptcies. That said,

it’s our opinion that the money behind many of these entities is fairly

intelligent and there will also be restructurings, mergers and acquisitions

that will make the overall industry that much more efficient and productive.

Have the Saudis miscalculated the impact of lower crude prices on US

production? – Sober

Look: “The Saudi response was quite

rational. Rather than cutting production to support crude oil prices, the

Saudis announced that output will remain the same. In private they were

planning to actually increase production in order to meet rising domestic

demand as well as to regain market share. The idea was to put a squeeze on the

high-cost North American oil firms, halting production growth and ultimately

getting prices back into a more profitable range. Other OPEC nations

reluctantly agreed to play along. Is it working? So far the results have been

less than what the Saudis had hoped for. After a bounce from the lows, crude

oil has been trading in a relatively tight range, with WTI futures fluctuating around

$60/bbl. How is this price stability possible when the common wisdom was that

oil prices below $70/bbl will force most US producers to close shop and North

American production would collapse? After all we've seen a spectacular decline

in active oil rig count. The answer has less to do with rigs that have been

taken offline and more with the technology that remains. After the inefficient

rigs have been shut, US rig count is starting to stabilize. US crude producers

are achieving record efficiency with the remaining equipment. The charts below

show new-well oil production per rig. From multi-well padding (multiple wells

in a single location) to superior drill bits, technology is helping to keep

production levels high. Well completion costs and the speed of drilling have

improved to levels many thought were not possible.”

U.S. Winning Oil War

Against Saudi Arabia – Forbes:

“In fact, I think they’ve lost this war

by inadvertently making the U.S. shale oil industry leaner and meaner. Most

likely, oil prices will remain reasonably low at somewhere around $70/bbl, and

natural gas prices quite low at about $3.75 per mmcf, for many years – which is

good for the American consumer, even if it might be bad for the environment.

From a production standpoint, this oil war pits conventional oil against

unconventional, sort of like jelly donuts versus tiramisu (see figure below).”

“While over half of

the proven oil reserves are generally under the control of OPEC, there are many

more unconventional reserves, such as oil shale, heavy oils and tar sands,

outside the Middle East (see 2nd figure below). And most of these are on the

edge of affordability. Thus, OPEC would like to keep the price of oil low

enough that these reserves never enter the world supply to jeopardize OPEC’s

influence.”

“However, while Saudi

Arabia produces 10 million barrels of oil per day, more than any other country,

it has little-to-no extra capacity to adjust to sudden increase in demand.

Similarly for the other OPEC nations. So

OPEC can no longer control the price and supply as well as they used to,

because there is too much outside supply and too much growing volatility in

demand. The above costs are only to sell from existing fields. But the Saudis

need over $100 per barrel to significantly grow their capacity to produce, a

critical distinction that is usually overlooked. So the Saudis pressed the OPEC

nations to drop prices by increasing production in the hope of driving U.S. oil

companies out of business. The big global oil companies could weather this war,

but the small ones, some of which led the fracking revolution, may not. What

this war has engendered, instead of halting U.S. shale oil production, is a

rapid consolidation and merging of companies that has increased efficiencies

and lowered production costs so that the marginal cost of shale oil can go

lower and lower and still allow shale oil to compete on the global market.

Zusman put it this way, “This behavior is typical for a new market that is

highly fragmented and inefficient, and that is undergoing a significant

evolutionary change. It is all about localizing, not generalizing, everything

from oil recovery, cost of full field development, and expected returns. There

is going to be a ton of performance dispersion as the industry moves into a

more manufacturing-like state. The race for land has now become a race for efficiencies.

“On the other hand, “In response to lower oil and natural gas prices,

exploration and production companies have slashed capital budgets by over 40%

on a year-over-year basis, and the oil rig count fell by 58% from its 2014

peak. ”Over 1,000 drill rigs in America, a third of all rigs that were active,

have been disassembled in the first half of this year (Oil&Gas 360). The

rig count fell at a pace of 57 rigs per week in the first quarter, faster than

the 49 rigs per week decline in 2009 when the financial world was collapsing. This

is just what OPEC was hoping for in their oil war with the United States, but

it does not seem to be accomplishing what they expected. The low prices led to

a global glut that led to the falling rig count, but without so many rigs, the

supply cannot rebound quickly and prices increased again, bringing more rigs

back. And the cycle repeats itself. With each iteration, the U.S. oil industry

gets more efficient and smarter. As an indication of this evolution, $11

billion of new equity was issued from the major oil companies in just the half

of 2015. This was more equity issued than in all of 2014, and means the capital

markets are available and ready and see a strong shale oil future. As all this

has been occurring within the United States, the rest of the world has been

changing, too. Dropping oil prices from $100/bbl to below $70/bbl has imperiled

the finances of many OPEC nations and authoritarian governments

overly-dependent on oil revenue. This, in turn, has produced social unrest,

since many of these governments are already at risk of violence from their

populations. Even worse for OPEC, the rate of change in oil production has

recently begun to slow, and the oil price has recovered from the low $40′s per

barrel to the mid $50′s. Five-year deferred oil futures contracts have

increased to $66 per barrel. This level can easily sustain the

newly-consolidated U.S. shale oil industry, effectively ending this oil war. Is

it time for the Saudis to surrender?”

US oil operators make

plans to add rigs, but will be disciplined: analysts – Platts:

“Several companies have already outlined

plans to add rigs, including:

--Pioneer Natural

Resources said, starting in July, it will put two rigs/month to work until

December. In Q1 2016 it expects to add eight more rigs, including six in the

eastern Permian and two in the Eagle Ford Shale. --Independent Matador

Petroleum could add a third rig in the Permian in the third quarter.

--Another small

independent, Parsley Energy, said it would accelerate one month, to June, its

addition of a fourth rig in the Permian Basin, on top of two others added

recently.

--WPX Energy said

Thursday it will add two more rigs in the Permian Basin starting in August.

--Apache reportedly

has indicated it may add five rigs, probably in the Permian, in second-half

2015 based on an oil price of $60-$65/b.

"While the

incremental [increases] may be scaring off some investors, the total amount of

additional committed rigs is roughly 40, which ... is not the game-changer that

should result in big changes in oil production trends," RBC Capital

Markets analyst Leo Mariani said in a Thursday investor note. One reason oil

companies may be slower to add rigs than they have been in the past is that

they have wrung astonishing efficiencies from their operations in a very short

period of time, as the number of days to drill a well keeps contracting while

initial well production rates and estimated hydrocarbon recoveries expand.

Also, corporate efficiencies, coupled with cost concessions of around 15%-25%

granted by oil services and equipment providers this year, have also lowered

well costs and driven up internal return rates in the best plays to the point

that operators appear comfortable with the current price environment, even if

they privately hope for an eventual return to $80/b oil. As long as operators

continue to pursue efficiencies, drive down costs and wrest larger volumes of

oil and gas from the ground to meet production goals, more rigs may not be

needed for awhile, said Carl Larry, a Frost & Sullivan oil and gas

consultant. "There's really no need to increase the rig count as long as

we're being as efficient as we are," Larry said. He added if oil should

hit $70/b it might be a catalyst to bring more rigs into the market.”

So U.S. drillers are adapting to changes in the underlying

pricing structure and again, that can have a profound impact on investments in

this sector at these levels.

Pessimism Amongst Oil

Traders Reaches 5 Year High – OilPrice.com:

“Even the oil majors are making big-time

cutbacks. From the largest oil companies alone, more than $200 billion in

spending on new oil projects have been cancelled or suspended, according to a

new Wood Mackenzie report. Those 46 projects account for 20 billion barrels of

oil reserves. Many of the projects are large-scale offshore projects located in

the Gulf of Mexico and off the coast of West Africa, but also high-cost onshore

fields, such as Canada’s oil sands. These projects require large upfront costs,

require complex engineering, and take years to develop. Royal Dutch Shell is

expected to announce fresh spending cuts this week, slashing several billion

dollars off of its $33 billion spending plan released in April. Deferring

projects today makes sense as oil companies try to plug deep holes in their

balance sheets. But it also raises the question over available supplies over

the long-term. Cancelling projects now will “create a substantial hole in the

industry’s investment pipeline,” the Wood Mackenzie report concludes. But that

is too far off for companies to think about. For now, many are just trying to

survive the latest downturn in prices.”

OPEC Pressures

The Saudi strategy is not only hurting the U.S. energy

market but other OPEC members as well. Perhaps internal OPEC members will have

sway over Saudi Arabia’s pricing strategy that Saudi Arabia may consider in

order to keep OPEC relevant in influencing oil pricing. In fact, the price of

oil rallied last week on unconfirmed rumors that Saudi Arabia was considering

production cuts later this year. Whether this influence is enough to alter the

current strategy remains to be seen, but there are certainly internal pressures

by other OPEC members.

The return of Iranian

oil might cause more tensions in OPEC – Business

Insider: “Richer Gulf producers, led

by OPEC kingpin Saudi Arabia, remain eager for the cartel to preserve valuable

market share and force out high-cost US shale producers with lower oil price levels.

“Clearly there is a divide between the countries on this new policy of seeking

new market share," Ann-Louise Hittle at consultancy Wood Mackenzie told

AFP. "So it could be a contentious (OPEC) meeting and there could be

pressure for an emergency meeting before December. “Faced with stubbornly low

prices, Algeria's energy minister Salah Khabri indicated to state news agency

APS last week that an emergency OPEC meet could be needed. "The real

problem starts when OPEC members begin to fight for quotas amid oversupply and

market share disputes," said Jassem al-Saadun, head of Kuwait's Al-Shall

Economic Consultants. "If Iran, Venezuela, Algeria and Libya -- all of

which need to pump more -- enter into a dispute with the Gulf producers, then

it could be the end for OPEC," he warned. Danske Bank analyst Jens Naervig

Pedersen said such countries had been "really hit" by low oil prices.

But he added: "Their collective power is probably not great enough to turn

the mind of Saudi Arabia and the core members of OPEC in the Middle East."”

Why We’re Building

Positions Now

Our sector rotation program attempts to place a fair market

value for each of the S&P sectors using income statement, balance sheet and

statement of cash flow variables. Each ratio is expressed as a “yield” and

correlations are run to assign the greatest weight to the valuation method that

has been most accurate historically. Running a historical back test of the methodology

has produced good returns. We found that the greatest average annual returns

can be found in the top three sectors that offer the greatest value. Over the

past fifteen years following a strategy that invests in the top three sectors

that yielded the greatest value with quarterly rebalancing produced results of

90.2% versus 44.7% for the S&P 500. The maximum drawdown (assuming zero

portfolio protection) for the program was 37.1% versus 53.5% for the S&P

500. The Sharpe ratio for the program produced a superior 3.36 compared to 2.26

for the index.

The S&P Energy sector currently ranks in the top three “valuable”

sectors.

Technical Mess

Looking at the weekly chart for WTI, it appears an important

near-term support level is approaching that may provide a spring of positive

buying with in the space. We also like to track the percent of companies within

the index that are in a point & figure bullish pattern as a sign for near

term strength. Currently 14% of the companies in the S&P Energy sector are

showing bullish P&F formations. Historically speaking for this index, any

reading below 16% represents a buy signal.

That said, looking out at the longer-term pricing chart, it

looks terrible. It is definitely plausible to expect the price of oil to retest

the late 2008 – early 2009 lows of sub $40ppb. As long as the RSI and stochastic

oscillators remain in a downward trend, portfolio protection is a viable

strategy.

Bottom Line: The

supply – demand dynamic surrounding oil appears broken and stocks are

reflecting that. With sentiment in the sector so low and with so many unknowns

within the supply – demand dynamic, it is our belief that much of this

negativity is already reflected in stock prices and any signs of positive news

within the space are bound to have exponentially positive implications for the

sector both psychologically and fundamentally. We are well aware of the risks

to our thesis and wouldn’t be surprised by further downside. We are unable to

pick the bottom but will do our best to mitigate losses in the portfolio. As we

await the coming support level, we will use any bounce in the space to add to

our portfolio protection as we wait for our fundamental thesis to take shape

(we don’t mind sacrificing a small portion of the expected return for portfolio

insurance at this point). Additional weakness will allow us to further increase

our position to our desired exposure.

Joseph S. Kalinowski, CFA

Additional Reading

Crude oil

has turned green – Business Insider

Here's why

the rig count matters – Business Insider

Halliburton is still getting slammed by

the oil crash – Business Insider

Actually, Iraq is the oil market's biggest

problem –

Business Insider

US banks are setting aside more money to

cover bad loans to energy companies – Business Insider

Oil Shipments By Rail Declining – OilPrice.com

The oil crash has done nothing for America – Business Insider

Sudden Drop in Crude-Oil Prices Roils U.S.

Energy Firms’ Rebound – Wall Street Journal

Are lower oil prices really a problem? – Calafia Beach Pundit

Oil Majors Resigned To Lower Oil Price

Environment – OilPrice.com

Chevron profits collapse – Business Insider

Exxon Mobil profits crash 52% - Business Insider

Historic Deal With Iran Opens Up Oil

Industry –

OilPrice.com

Crude oil is spiking – Business Insider

One of

the world's biggest oil companies thinks the worst is over – Business Insider

Drilling

giant Baker Hughes warns the pain from oil crash is far from over –

Business Insider

No part of this report may be reproduced in any manner without the expressed written permission of Squared Concept Partners, LLC. Any information presented in this report is for informational purposes only. All opinions expressed in this report are subject to change without notice. Squared Concept Partners, LLC is an independent asset management and consulting company. These entities may have had in the past or may have in the present or future long or short positions, or own options on the companies discussed. In some cases, these positions may have been established prior to the writing of the particular report.

This analysis should not be considered investment advice and may not be suitable for the readers’ portfolio. This analysis has been written without consideration to the readers’ risk and return profile nor has the readers’ liquidity needs, time horizon, tax circumstances or unique preferences been taken into account. Any purchase or sale activity in any securities or other instrument should be based upon the readers’ own analysis and conclusions. Past performance is not indicative of future results.

No comments:

Post a Comment