The market bounced off the lows from last Monday and offered

a trading opportunity for those aggressive traders that chose to capitalize on the

recent volatility. As of this writing at 1 am Monday morning, it appears the

Asian markets are trading lower and U.S. futures are indicating a lower open.

Last week we wrote that we expected a near-term bounce but expected the market

to continue lower. We believe the technical damage to the market over the past

several days is fairly severe. Investor sentiment may be turning increasingly

negative, momentum is weak and the markets remain overvalued in our opinion. We

believe it is possible for the S&P 500 to retest the lows from last year at

around $1820 over the next several months. We will trade the market to the

downside by shorting over-bought situations until there is improvement in the

sentiment/momentum picture.

The Next Bear Market

There has been a significant amount of discussion on whether

this is a classic correction (+10% stock market decline) or the start of

something more sinister. The accepted definition of a “bear-market” is a +20%

decline from the peak of a specific index. I came across this interesting piece

from JP Morgan (Via Business

Insider) that profiled the start of historical bear markets. The article

states, “JP Morgan's review of global

markets and economies included a look back at the past ten bear markets in US

history, dating back to the Great Depression. To qualify, S&P 500 had to drop

20% off the all-time high. Looking at the slide, there are some themes that pop

out. Maybe most obviously, 8 of the 10 were accompanied by recessions as

defined by the National Bureau of Economic Research. The three main hallmarks

JP Morgan observed — commodity spikes, aggressive Fed tightening and extreme

valuations — each occurred four times over the 10 bear markets and only once,

the 1987 crash, bore none of those hallmarks. Commodity spikes (defined as

"significant rapid upward move in oil prices") and aggressive Fed

tightening ("monetary tightening that was unexpected and significant in

magnitude") occurred together 3 times and is what JP Morgan cites as

conditions during the 2007 Global Financial Crisis. While it may simplify broad

economic situations, the chart provides an intriguing snapshot of when and why

US markets meltdown.”

We firmly believe, based on the data that we currently have

that this is a market correction and not the start of a new bear market. The

leading economic indicators that we track are showing slow but stable growth,

so it doesn’t appear an economic recession is on the horizon. The Fed is going

to start a tightening cycle but given the ultra-easy monetary policy in place,

a small increase in rates doesn’t appear to be a threat to the market.

Commodities are not spiking, in fact quite the contrary the sector has been chronically

weak.

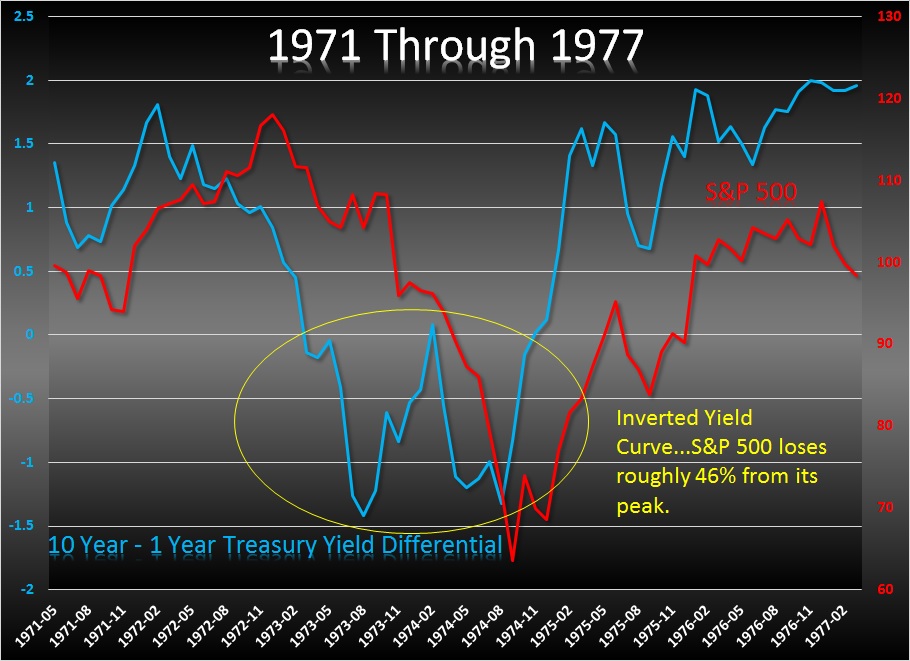

Perhaps the most important item we track is the yield curve.

Typically the yield curve will become inverted when economic growth is

threatened and the stock market is weakened. I have listed previous points in

history when the yield curve had become inverted and subsequent market under

performance. The last chart of this series shows where we are today and quite

frankly it doesn’t appear to be a major threat signifying a bear market – yet. We’ll be watching closely.

Bottom Line: We

expect additional market weakness once this market bounce concludes, possibly

through September and October. We may see the S&P 500 retest the levels hit

in October of last year. We would like to see valuations come in line and

sentiment improve and are hopeful of a renewed rally as we head into the end

of the year. Given the current data, we do not see this turning into a severe

bear market but will be watching the data closely.

Joseph S. Kalinowski, CFA

Additional Reading:

Does

stock market decline signal a recession? – The San Diego Union-Tribune

This

is 'the danger' – Business Insider

US

consumers aren't too worried about the stock market's wild ride – Business Insider

STOCKS

FINISH THE WEEK HIGHER: Here's what you need to know – Business Insider

TOM

LEE: Here are 4 reasons to 'stay bullish' – Business Insider

ALBERT

EDWARDS: There's a 99.7% chance we're in a bear market – Business Insider

'This

doesn't look like a slowing economy to me' – Business Insider

The

Problem Now Is The Overhead Supply – All Star Charts

As

Market Mayhem Grips Investors, Fewer Americans Have A Stake In What Happens On

Wall Street – International Business Times

Forget

about the market for a second, and remember the US economy is kicking butt –

Business Insider

Can

US Economy Weather the Global Storm? – Dr. Ed’s Blog

TOM

LEE: History shows that we're not doomed for a bear market – Business Insider

Strategist:

The Market Selloff Has Nothing to Do With the U.S. Economy – Bloomberg Business

Finding

Buy Points With Moving Average Ratios – Traders Narrative

No part of this report may be reproduced in any manner without

the expressed written permission of Squared Concept Partners, LLC. Any information presented in this report is

for informational purposes only. All

opinions expressed in this report are subject to change without notice. Squared Concept Partners, LLC is an

independent asset management and consulting company. These entities may have

had in the past or may have in the present or future long or short positions,

or own options on the companies discussed.

In some cases, these positions may have been established prior to the

writing of the particular report.

The above information should not be construed as a

solicitation to buy or sell the securities discussed herein. The publisher of this report cannot verify

the accuracy of this information. The owners

of Squared Concept Partners, LLC and its affiliated companies may also be

conducting trades based on the firm’s research ideas. They also may hold positions contrary to the

ideas presented in the research as market conditions may warrant.

This analysis should not be considered investment advice and

may not be suitable for the readers’ portfolio. This analysis has been written

without consideration to the readers’ risk and return profile nor has the

readers’ liquidity needs, time horizon, tax circumstances or unique preferences

been taken into account. Any purchase or sale activity in any securities or

other instrument should be based upon the readers’ own analysis and

conclusions. Past performance is not indicative of future results.

No comments:

Post a Comment