Even excluding auto sales and gas the numbers were soft (although the March figures were revised higher). Looking at the year-over-year growth in retail sales there appears to be a pretty solid downtrend at this point which is disappointing considering the fall in gasoline prices were supposed to provide a shot in the arm for retailers. Now gas prices are on the rise with AAA saying, “The national average price of gas has increased for 26 of the previous 27 days to $2.66 per gallon, which is the highest average of the year.” That doesn’t seem like a positive trend.

According to the preliminary University of Michigan Consumer

Confidence figure, the U.S. consumer – the backbone to this country’s economic

growth prospects - is losing confidence in the economy. In light of the

expected “rebound” from the abysmal 1Q15 weather related softness, consumer

confidence registered 88.6 in May, way off from the expectations of around

95.9.

Richard Curtin, the chief economist for the Michigan survey

stated (via

Business Insider), “Confidence fell in early May as consumers became

increasingly convinced that there would be no quick and robust rebound

following the dismal first quarter (even if the underperformance was

exaggerated by inadequate seasonal adjustments)."

So are we headed for a severe economic slowdown or quite

possibly a recession?

The Atlanta Fed had quite a bit of press last

quarter after accurately predicting soft 1Q GDP when the rest of consensus were

clinging to overly optimistic expectations. Impressive work and something worth

watching. That said, they are at it again calling for just 0.7% economic

growth while consensus is still sitting around 3.0% expected growth.

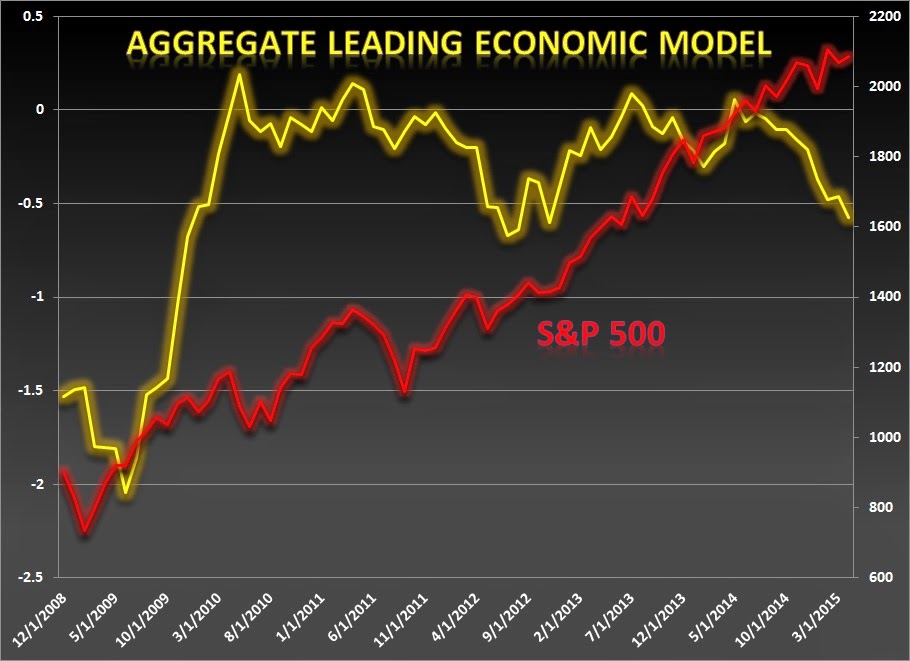

When tracking the economy, I like to aggregate several leading indicators into a single easy to read economic gauge. The variables that I input into the model are U.S. Average Weekly Manufacturing Hours, U.S. Manufacturers New Orders Consumer Goods, the Conference Board U.S. Leading Index Vendor Performance, the Conference Board U.S. Manufacturers New Orders Non-Defense Capital Goods, M2 Money Supply and University of Michigan Consumer Expectations. The chart below places this model against the S&P 500. The trend for the economic model is trending lower and yet the S&P 500 remains unfazed by the seeming economic slowdown. The stock market is the ultimate leading indicator and I always default to the market knows best discipline but this divergence is worrisome (the last time such a divergence occurred was the 2011 market correction).

The Citigroup Economic Surprise Index is also showing how

far the general economic consensus is off from reality. This index isn’t

exactly a pure reading on economic growth but more of a reading of economist

forecasts versus the actual economic releases. It is telling us that the

forecasts that are published are probably too optimistic and need to be

trimmed.

Climbing the Wall of Worry

April 30, 2015 CNBC

– “Marc Faber: Stocks are about to fall

40%—at least! “The market is in a position where it's not just going to be a 10

percent correction. Maybe it first goes up a bit further, but when it comes, it

will be 30 percent or 40 percent minimum!" Faber asserted. Faber says low

yields and stimulative central bank policies around the world have led to a

condition in which "all assets are grossly overvalued … and eventually

this will unwind and cause some problems."”

April 30, 2015 CNBC

– “It's going to get ugly, says Dennis

Gartman. "It's not going to get ugly bad; it's not going to get ugly for a

long period of time. I think it's going to get ugly swiftly and I think it's

going to make a lot of people very nervous," the editor and publisher of

The Gartman Letter said in an interview with CNBC's "Closing Bell" on

Thursday. He expects the downturn to last two to three weeks, and said then

it'll be time to buy again.”

May 1, 2015 CNBC

– “Mario Gabelli: There's no margin of

safety in stocks. “As we look into 2016 ... I'm [also] looking at the economy

in Europe picking up. The American companies will do a lot better because of

earnings in Europe coming into the U.S.," he predicted in a CNBC

"Squawk Box" interview. "The [U.S. stock] market is a function

of earnings, and we're comfortable with that." He warned, however, that

"on balance there's no margin of safety. If something goes wrong, you'll

have the volatility that you had [Thursday]." The Dow Jones Industrial

Average, the S&P 500, and the Nasdaq Composite Index closed lower in a

choppy session on the final trading day of April, which did finish positive,

but just barely.”

May 4, 2015 Business

Insider – “We haven't heard Carl

Icahn this bearish in a long time. He told hosts Anthony Scaramucci and Gary

Kaminsky that his portfolio was hedged for a correction. "I'm very

concerned about the market," he said. "I think that you have a

situation where this market keeps going up ... and yet a lot of the economic

news isn't all that good, and also more importantly, earnings aren't

good." The bottom line, to Icahn, is that some stocks are trading at 17

and 18 times the S&P. Those same stocks are going to whiff earnings. What

rational person would buy that?”

May 4, 2015 Business

Insider – “BUFFETT: Stocks won't look

cheap if interest rates rise. Stocks are definitely on the "high side of

valuation," Berkshire Hathaway CEO Warren Buffett says.”

May 4, 2015 Monthly Investment

Outlook from Bill Gross – “Policymakers

and asset market bulls, on the other hand speak to the possibility of

normalization – a return to 2% growth and 2% inflation in developed countries

which may not initially be bond market friendly, but certainly fortuitous for

jobs, profits, and stock markets worldwide. Their “New Normal” as I reaffirmed

most recently at a Grant’s Interest Rate Observer quarterly conference in NYC,

depends on the less than commonsensical notion that a global debt crisis can be

cured with more and more debt. At that conference I equated such a notion with

a similar real life example of pouring lighter fluid onto a barbeque of warm

but not red hot charcoal briquettes in order to cook the spareribs a little bit

faster. Disaster in the form of burnt ribs was my historical experience. It

will likely be the same for monetary policy, with its QE’s and now negative

interest rates that bubble all asset markets.

But for the global

economy, which continues to lever as opposed to delever, the path to normalcy

seems blocked. Structural elements – the New Normal and secular stagnation,

which are the result of aging demographics, high debt/GDP, and technological

displacement of labor, are phenomena which appear to have stunted real growth

over the past five years and will continue to do so. Even the three strongest

developed economies – the U.S., Germany, and the U.K. – have experienced real

growth of 2% or less since Lehman. If trillions of dollars of monetary lighter

fluid have not succeeded there (and in Japan) these past 5 years, why should we

expect Draghi, his ECB, and the Eurozone to fare much differently?”

May 6, 2015 Bloomberg

Business – “Yellen Says Stock

Valuations ‘Quite High,’ Bond Yields Low. Federal Reserve Chair Janet Yellen,

surveying the financial landscape for signs of bubbles after more than six

years of near-zero rates, warned that both stocks and bonds are richly valued.”

“I would highlight that equity-market valuations at this point generally are

quite high,” Yellen said in Washington on Wednesday in response to a question

at a forum on finance. “Now, they’re not so high when you compare the returns

on equities to the returns on safe assets like bonds, which are also very low,

but there are potential dangers there.””

May. 8, 2015 Seeking

Alpha – ”Signs Of A Stock Market

Correction Developing - My view is that price action in the stock market is

hinting at some possible "changing winds" in the days, weeks and

months ahead. If the break of the ascending triangle in the short-term chart is

confirmed, and if the market subsequently breaks and confirms a break of the

lower channel trend line in the longer-term chart (the break has not happened

yet), I think the market may be set up to enter into a corrective phase.”

- James A. Kostohryz.

May 12, 2015 Business

Insider – “HARRY DENT: 'The curtains

are falling for the greatest bull market and bubble in history' - We’ve been in

an unprecedented period since late 2008 wherein central banks around the world

have stepped in and printed whatever amount of money they deemed necessary.

They’re desperately trying to stop the depression and deflation meltdown that

started in the second half of that year.

But there is a limit

to how much you can stimulate an economy pointing down… especially one already

up to debt levels twice that of the last great bubble boom that peaked in 1929

— 4 times if you include unfunded entitlements. Just how much more can you get

people and companies to spend and borrow when they already way overdid that? The

answer is, you can’t.”

Risk Management

There is always the treat of a correction or bear market on

the horizon but it is truly impossible to forecast when it will happen. In the

cases of market “bubbles”, market sentiment has much more influence on asset

prices than intrinsic values. Attempting to time market tops and bottoms is a

futile and unprofitable strategy in my opinion. Understanding the fallacy of

the Efficient Market Hypothesis and the Efficient Frontier and embracing the influence

investor behavior can have on market valuations is one of the hardest parts of

investing.

We have written in the past about our concerns about the market

valuation but have an equally sound concern about missing potential market

gains by ignoring the power of investor sentiment. The proper use of portfolio

risk management while maintaining equity exposure is the most prudent option

right now, in our opinion. Building cash from dividends and interest and the

use of options is reasonable. We acknowledge providing liquidity using call

options on our positions in the near-term and taking liquidity using put option

on our positions on a longer term prospective will create a collared strategy

that will minimize the damage should a sudden shift occur. This strategy also

keeps the portfolio insurance costs under control.

With the proper risk management in place, we are not only

prepared for a correction but actually encourage it. When following a concave

constant mix portfolio structure, it allows us to reposition the holdings in

the portfolio to take advantage of new opportunities. Most of the alpha

generated within the portfolio comes from such events in our experience.

Joseph S. Kalinowski, CFA

No part of

this report may be reproduced in any manner without the expressed written

permission of Squared Concept Partners, LLC.

Any information presented in this report is for informational purposes

only. All opinions expressed in this

report are subject to change without notice.

Squared Concept Partners, LLC is an independent asset management and

consulting company. These entities may have had in the past or may have in the

present or future long or short positions, or own options on the companies

discussed. In some cases, these

positions may have been established prior to the writing of the particular

report.

The above

information should not be construed as a solicitation to buy or sell the

securities discussed herein. The

publisher of this report cannot verify the accuracy of this information. The owners of Squared Concept Partners, LLC

and its affiliated companies may also be conducting trades based on the firm’s

research ideas. They also may hold

positions contrary to the ideas presented in the research as market conditions

may warrant.

This analysis

should not be considered investment advice and may not be suitable for the

readers’ portfolio. This analysis has been written without consideration to the

readers’ risk and return profile nor has the readers’ liquidity needs, time

horizon, tax circumstances or unique preferences been taken into account. Any purchase

or sale activity in any securities or other instrument should be based upon the

readers’ own analysis and conclusions. Past performance is not indicative of

future results.