It’s been quite a week for investors as sentiment has

decidedly turned negative. The trick is not to panic. Two weeks ago we decided

to add portfolio protection in our program portfolios. We wrote in our blog on

August 9th entitled Time to Consider Portfolio Protection, “Market fundamentals are signaling

over-valuation and market sentiment/momentum appears to be weakening. This

along with less accommodative monetary policy on the horizon increases the risk

of a market correction, in our view. We will maintain our existing portfolio

but will start introducing “portfolio insurance” in the coming weeks and months

as the market dictates. It is impossible to predict market tops and bottoms but

it is prudent to alter the risk profile of the portfolio with changes in market

data. We’d rather risk a portion of future upside if we are wrong in our

analysis than risk previous gains if we’re right.”

We are fortunate to not have suffered major losses in our

program portfolios and our more opportunistic portfolio is decidedly positive

month-to-date. Given the recent action, it’s now time to review our positions

and continue to build upon our investment thesis.

Short-term Action

We are expecting the market to stage some sort of rebound

from its current level. In the figure below, we are seeing what I would

describe as fairly rare opportunities. On Friday, the spot and future prices

for the VIX inverted and that ratio shot above one. This usually signifies a

near-term market bottom. The Put – Call ratio spiked to 1.69. Anything above

1.4 also indicates near-term overreaction and a possible bounce in the market.

Lastly, the VIX itself rallied over 100% in the past five trading days. When

looking at the second derivative rate of change for the VIX, anytime there is a

big upward spike in such a time frame, it usually indicates a near-term buying

opportunity. In fact, going back to 1990 there have only been 31 cases in which

the VIX spiked over 50% in five trading days. In 27 of those cases (87% of the

time) the market traded higher over the next five trading days with an average

gain of 3%.

Staying with the S&P 500 as a benchmark, both the RSI

(5) and fast stochastics are signaling extreme oversold conditions. We would

expect the market to rally to the top of the shaded range in the following

figure or roughly 2020. Depending on the strength of the rebound we may see the

market advance further to 2040 which appears to be the base of the neckline

that started earlier this year. Beyond that the next resistance level may be

the 200-day moving average of 2077 but I’m doubtful that level will be reached

given the severity, volume and technical damage of this sell-off. We will see

how trading next week starts and if we see stabilization and upward action on

the daily MACD histogram, we will take profits on the equity put options that

we introduced to the portfolio. For our more opportunistic clients, we will be

looking to trade the bounce.

Intermediate – Term

Action

That said, weekly and monthly momentum is decidedly negative

for the SPX and portfolio insurance is a fact of life for the foreseeable

future. We believe the stock market will continue lower after the short-term

bounce described earlier. We will be looking for a few things. We would want to

see (1) the RSI (5) and fast stochastics reach overbought levels, (2) one of

the three test points mentioned earlier provide verifiable resistance and (3)

daily MACD histogram resume lower. If those events were to happen, we will

reposition ourselves with the appropriate downside protection and look for

additional market weakness.

We have written in the past that fundamentally it appears

the market is overvalued and is due for a correction. (See The

Coming Market Correction?) We did not know what the catalyst would be to

start the correction as investor sentiment remained bullish. We commented that

a possible cause of the coming correction may be unsettling headlines out of

China. It appears that may be happening. An article in CNN Money entitled - China's

economy is in trouble. How bad is it? ; states two sides of an argument.

They write, “There is almost no way that

China's economy is growing as well as the government says it is. For years,

experts have questioned whether China cooks its books. "The question is

not whether they're right, it's how wrong are they," says Derek Scissors,

an Asia expert at the American Enterprise Institute. But you don't need a PhD in statistics to

figure it out this time. Just take a look at what China's government has been

doing lately: making a surprise devaluation of the yuan in an effort to boost

exports, propping up its markets by actually buying stocks, spending big and

cutting interest rates in an effort to stimulate its economy. China wouldn't be taking these actions if

the country really was chugging along at the 7% growth rate that the latest

government data claims. "China could be in the world's greatest

depression and they would still report 7%," says Gordon Chang, a China

expert and author of “The Coming Collapse of China." (Emphasis added)

They go on to compare two popular arguments on the Chinese

economy:

“Here's the case for a

2% vs. 5% growth scenario:

1. It's a major

slowdown. Chang says he has heard that in Beijing, they are privately talking

about 2% growth. He's not surprised. Across the board, the statistics don't

look good with everything from steel to rail freight to electricity consumption

showing big drops. China's manufacturing sector looks especially weak --

sentiment just hit its lowest level in six years.

"There's a lot

there that looks really wrong," says Chang.

While Chang

acknowledges that China is taking various stimulus measures, he is concerned

that a lot of the growth is coming from people, companies, real estate

developers and even local governments taking on more debt. "The growth

they are creating is crap growth," says Chang. "They're aggravating

their debt problem and they have no solution." He estimates the true GDP

number is likely 1% to 2% growth. Expect China to hurt American company

earnings for the rest of the year. Even worse, expect more panic "because

people think that China is more important than it actually is."”

Or…

“2. It's a minor

hiccup. Other experts say that predictions of a "hard landing" in

China go too far.

"This is not

2009," says Scissors, the America Enterprise Institute scholar. He

estimates GDP is growing at about 4.5%. Global forecasting company Capital

Economics has traded jabs with the Chinese government before over the validity

of the government statistics. Capital Economics believes China is likely

growing at 5% to 6%. China's economy probably did a lot worse than what it

reported in the first half of the year, but there could be a pickup in the

second half, especially as all of the stimulus measures take root. "There

are signs the economic conditions are improving," says Mark Williams,

chief Asia economist at Capital Economics. He reminds people that growing at 5%

to 6% isn't the "very dark place" some are warning about. Another key

for Americans to remember is that when the Chinese get nervous, they tend to

invest their money abroad. "Bad Chinese economy performance means more

Chinese money leaving their country, and the No. 1 place it comes is

here," says Scissors.”

What stands out to me is that the argument has shifted from

a “grow vs. slow” debate to “slow vs. even slower” one. A slowing Chinese

economy certainly has profound implications on our economy and equity markets

but it’s yet too soon to know if this will result in a U.S. market correction

or the groundwork for the next “big – one” bear market.

This turmoil is definitely reflected in asset prices in Asia.

According to Arthur Hill at StockCharts.com,

“SHANGHAI COMPOSITE BREAKS LONG-TERM

MOVING AVERAGE... Chart 11 shows the Shanghai Composite ($SSEC) moving below

its 50-day moving average, stalling and then breaking its 200-day moving

average. A triangle formed to mark the consolidation over the last two months

and this is a consolidation within a downtrend, which is typically a bearish

continuation pattern. With a close at 3507 on Friday, the index broke the

200-day and triangle support to signal a continuation lower. Chart 12 shows the

X-Trackers China A-Shares ETF (ASHR) breaking support in late June, bouncing

back to 44 and breaking down again this week.”

For the purposes of our intermediate investment strategy we

will assume recent market action as the start of a potential market correction

(down 10% from its peak) vs. a bear market (down 20%). A keen eye on portfolio

protection and defending previous gains is warranted as we wait and see if

investor sentiment has truly taken a turn for the worse.

Speaking of Investor

Sentiment

In an interview with CNBC,

Robert Shiller stated the following on the contagious effects of negative

investor sentiment. They write,”Nobel

Prize-winning economist Robert Shiller has warned for months against being

overexposed in an overheated market. And with the major U.S. averages pacing to

cap their worst week of the year Friday, it certainly appears to be a

well-timed caution, but Shiller isn't saying it's over yet. "It could be

followed by even bigger and bigger moves," he told CNBC's "Squawk on

the Street" in an interview. "I have a general bias towards down

because the market is overpriced, but these things unfold over years."

While Shiller conceded the possibility that the selloff could "create

aftershocks in either direction in the short-term," he highlighted a

psychological bias for those in the periphery to "over focus on the latest

news." "When people who don't normally pay attention to the market

are brought in, it can feed on itself like an epidemic," he said.”

The Case for a

Correction

Negative headlines out of China and the potential of

investor pessimism spreading has us looking at fundamental valuation once

again. Several weeks ago we wrote, “Based

on Bloomberg data, the companies that comprise of the S&P 500 are expected

to show $125.71 in earnings per share over the coming twelve months and have a

current earnings yield of 6.1%. Book value per share for the index is $736.68

with a BV yield of 35.4% and cash flow per share of $180.23 for a CF yield of

8.8%. If we weight each valuation measure according to accuracy in predicting

future price movements our blended fair value for the S&P 500 is $1702 or

about 18% overvalued.”

We are of the opinion that the combination of negative news,

deteriorating investor sentiment and an overvalued market could be the genesis

of a +10% correction for the S&P 500. Other valuation measures outside of

our own paint a similar picture.

Henry Blodget, of Business Insider

writes this, “In the past year or two,

stocks have moved from being "expensive" to being "very

expensive." In fact, according to several historically valid measures,

stocks are now more expensive than they have been at any time in the past 130

years, with the exception of 1929 and 2000 (and we know what happened in those

years). The chart below is from Yale professor Robert Shiller. It shows the

cyclically adjusted price-earnings ratio of the S&P 500 for the past 130

years. As you can see, today's PE ratio of at least 26 is miles above the long-term

average of 15. In fact, it is higher than at any point in the 20th century,

with the exception of the months that preceded the two biggest stock-market

crashes.”

“What about other

valuation measures? Most of them paint the same picture. Here, for example, are

a few recent charts from Doug Short, one of the best market-chart makers

around. The first chart plots four valuation measures — the Shiller P/E ratio

above, another P/E ratio (different calculation), the "Q ratio" (a

measure of price to replacement cost), and a regression analysis for stocks

themselves. Same message: Averaging the four suggests that stocks are ~80%

overvalued.”

“And for good measure,

here's another ratio — one that is fondly referred to as "Warren Buffett's

favorite valuation measure." (Because he once said it was.) This one

charts the collective value of all stocks to the size of the economy (GDP). It

recently hit its second-highest level ever.”

More Evidence of

Intermediate Market Weakness – Credit Spreads

As this article in Fox

Business reports, “With the S&P

500 and the Dow Jones Industrials tossing away their gains for the year, bond

prices are rising in what could be a bad omen for U.S. stocks. Investors poured

$1.3 billion into U.S. Treasuries for the week ended August 19, the biggest

score since mid-April, according to data from Thomson Reuters’ Lipper. The

yield on the 10-year benchmark, which trades inverse to bond prices, is

hovering at 2.084% and has been on the decline since early July; and that trend

may continue according to Mary Ann Bartels, chief investment officer of

portfolio solutions at Bank of America Merrill Lynch Wealth Management (BAC).

“The 10-year yield is starting to break down, technically pointing to lower

lows, it could break 2% technically,” said Bartels on FOX Business Network’s

Mornings with Maria.”

“As bond yields fall

and bond prices rise, U.S. stocks are paying the price. As of Thursday, the

S&P 500 is down 1% for the year, the Dow Jones Industrials nearly 5% while

the Nasdaq Composite hangs onto its 3% gain. A big reason investors are

gravitating toward the safety of U.S. government debt is China. “Large

institutions are selling due to China.” said Jason Rotman, managing partner of

Lido Isle Advisors, while appearing on FOX Business Network’s Risk &

Reward.”

The standing divergence between credit spreads and stock

prices has been pointed out previously in this blog as the bond market has

been predicting a market correction from earlier this year. It is only now that

the stock market seems to be listening to the warnings from the bond market.

Negative Intermediate

– Term Momentum

The following graphic shows that long – term momentum has

turned negative, solidifying our belief that the stock market will continue its

downward move after the coming “bounce”. After a slight upward movement in the

SPX to the 2020 - 2070 level the market should offer additional shorting – portfolio protection

opportunities probably through September and October, in our opinion.

Is this the Big One?

The question will arise as to the magnitude of the

continuation of the sell-off. We do believe a market correction (down +10% from

the peak) is in order. We are not thinking a full blown bear market (down +20%

from the peak) is in the cards. Of course this is nearly impossible to predict

but our opinion is that all the intermediate problems mentioned above (negative

news out of China, overvaluation concerns and deteriorating momentum) will wash

out and the bull market will continue higher. We are anticipating a correction

within the bull market currently.

We just don’t see the signals that we are accustomed to

prior to a major downward movement in the stock market.

As Scott Grannis of Calafia

Beach Pundit points out, “For the

past several months, TIPS have been telling us that inflation expectations have

been declining—though only moderately: deflation is still nowhere to be found.

At the same time, the rise in real yields on TIPS tells us that the market is

expecting somewhat stronger growth—though still far less than enough to erase

the economy's huge output gap, which I estimate to be about $1 trillion per

year. It's a message that should do nothing to derail the Fed's plan to

normalize interest rates at a somewhat higher level, and it should do nothing

to provoke an outright tightening of policy. Slow and relatively stable growth,

accompanied by relatively low inflation, is not very exciting, but it's not

something to worry about either. It's supportive of continued, modest gains in

equity prices.”

“In the chart above,

the difference between the nominal yield on 5-yr Treasuries and the real yield

on 5-yr TIPS gives us an expected annual (CPI) inflation rate of 1.27% over the

next 5 years. This is relatively low compared to past history for this series,

but it is nowhere near the levels that reflect deflation risk, such as we saw

at the end of 2008.”

“As the chart above

shows, the recent decline in this same expected inflation rate over the next 5

years is driven by and large by the price of oil. Lower expected inflation is

not a symptom of tight money; it is the by-product of strong gains in oil

production. As such, this is a welcome development, since a lower cost of

energy enables a stronger economy.”

“As the chart above

suggests, the real yield on 5-yr TIPS tends to track the economy's growth rate.

Which makes sense, since the real growth of the economy sets an upper limit on

the real growth of its constituent parts. If the bond market is comfortable

with risk-free real yields of 0.3% for the next 5 years, then real growth in

the broad economy is quite likely to be somewhat higher. This year's increase

in real yields suggests that the market is pricing in a modest acceleration in

the rate of GDP growth over the next year or so. Nothing to get excited about,

but nothing to worry about either.”

I like to track trucking and rail shipments as a gauge of

economic activity. As we mentioned in our posting

on July 12, we are still seeing year-over-year growth in rail traffic, although

the numbers we track are provided quarterly so we will need to update this when

the September figures are released. Truck tonnage continues to show gains as

well. Back to the post by Scott Grannis, “The

physical weight of stuff carried by the nation's trucks increased 3.7% in the

year ending July. This is a pretty good indication that the economy is growing.

As the chart [below] shows, truck tonnage correlates reasonably well with the

real value of U.S. equities. As the economy expands, real stock prices

increase, which makes sense. The modest increase in truck tonnage in the past

years suggests that the stock market is not in a bubble (neither undervalued

nor overvalued), and is likely to increase modestly for the foreseeable future.”

The Atlanta Fed publishes its GDPNow

indicator that attempts to forecast quarterly economic growth. They have been

very accurate of late and it is something I have started watching on a

continuing basis. They write, “The GDPNow

model forecast for real GDP growth (seasonally adjusted annual rate) in the

third quarter of 2015 is 1.3 percent on August 18, up from 0.7 percent on

August 13. The forecast for real GDP growth increased from 0.7 percent to 1.2

percent after Friday's industrial production release from the Federal Reserve.

Most of this increase was due to a 15.3 percent increase in seasonally adjusted

motor vehicle assemblies in July that boosted the forecast of the contribution

of real inventory investment to third-quarter GDP growth from -2.2 percentage points

to -1.8 percentage points.”

The housing market remains firm as well. According to Tom Lee of Fundstrat (via Business

Insider): “The US housing market

recovery is the most important reason to still believe in the bull market,

according to Fundstrat's Tom Lee.”

“In a note to clients

on Friday, Lee wrote (emphasis and link added): "In our view, the most important element for remaining constructive is

the ecosystem benefiting from a US housing recovery. July

2015 housing starts rose to 1.206mm, reaching a 7-year high and further

confirmation of a broadening housing recovery which should lead to US housing

starts rising to 1.7-2.0mm (typical peaks) ... US residential construction is

3.3% of GDP but is expected to rise to at least 5.5% (1.7mm starts) and such an

increase would more than offset the 40% decline in Energy capex, which has

fallen from 1% of GDP to 0.6%. In fact, as we show, starts need to reach

1.374mm to fully offset the 40% decline in Energy spending, which could be seen

within 12 months." Lee says that although the past few weeks have been the

worst of 2015 for the stock market, his call for a longer-term rally, and the

2,325 year-end target on the S&P 500, is unchanged.”

Manufacturing continues to chug along despite weakening

figures of late. According to Markit

Economics, “U.S. manufacturers

indicated a renewed loss of momentum during August, with output, new business

and payroll numbers all increasing at a slower rate than in the previous month.

As a result, the headline seasonally adjusted Markit Flash U.S. Manufacturing

Purchasing Managers’ Index™ (PMI™)1 dipped from 53.8 in July to 52.9 in August.

The index remained above the neutral 50.0 threshold, but the latest reading was

the lowest since October 2013.”

The way I track manufacturing data is to combine all the

surveys into one z-score that is easy to read and quick to reference. The

aggregate manufacturing score combines ISM Manufacturing PMI, the Philly Fed outlook,

the Dallas Fed manufacturing survey, the Chicago Fed activity index, the Empire

State manufacturing survey, the Richmond Fed manufacturing survey and the

Cincinnati PMI. I think that just about covers this country’s manufacturing

sector. Outside of a strange divergence between the manufacturing figures and

the S&P 500 that started earlier this year (possibly correcting itself

currently) it appears the manufacturing sector continues to chug along as we

have seen for many quarters with no significant breakdowns showing. Of course

the market is the leading indicator in this case but further significant

weakness in this model would change our investment thesis as it relates to a

coming bear market.

Indeed many other economic metrics that we track are showing

slow but positive year-over-year growth. Further deterioration in these

economic models may sway our longer-term investment thesis but for now we are

going to assume the economy is not heading for a recession.

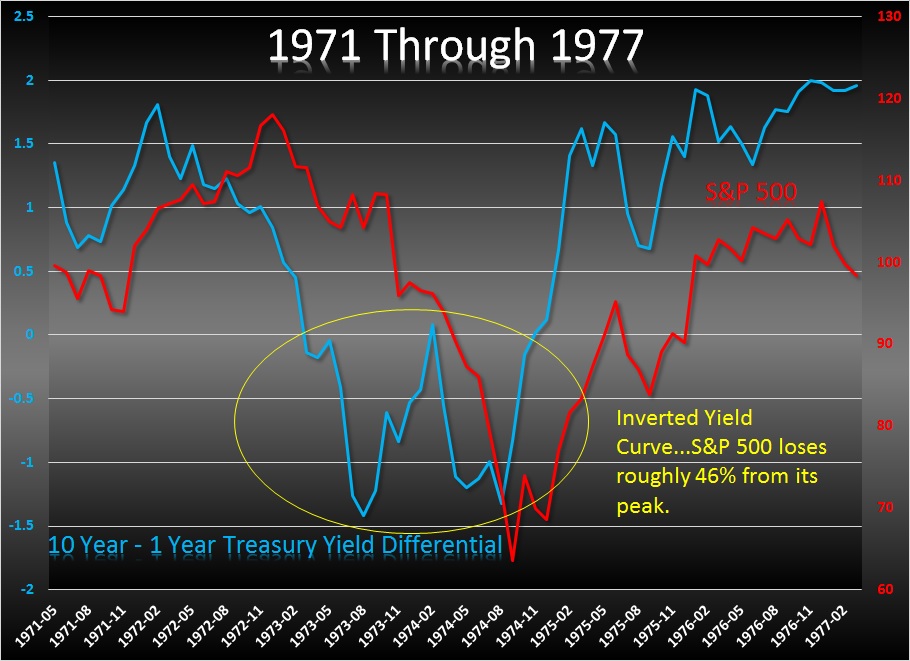

Monetary Policy

We understand the Fed’s desire to normalize monetary policy

and ween the market off of its multi-year ZIRP program. We watch the yield curve

(the spread between the two and ten year treasury yield) as our best gauge of

economic strength. An inverted yield curve is a dangerous sign for the stock

market and we were not all that concerned about the current positioning until recently. The flight

to quality is now driving the ten year yields lower just as the Fed anticipates

raising rates on the short end. If the model below gets to an inverted position

then we would definitely need to rethink our investment thesis but for the most

part it currently is not flashing a long-term economic warning.

Given the recent market weakness, many are speculating that

a Fed rate hike in September is off the table. From Business

Insider, “On Wednesday, we got the

much-anticipated minutes from the Federal Open Market Committee's July meeting.

However, they did little to support anybody's conviction about a September rate

hike. The minutes indicated that although the Fed saw the economy approaching

the conditions appropriate for a rate hike, members thought those criteria had

not yet been reached. From the minutes:

... The Committee

agreed to continue to monitor inflation developments closely, with almost all

members indicating that they would need to see more evidence that economic

growth was sufficiently strong and labor markets conditions had firmed enough

for them to feel reasonably confident that inflation would return to the

Committee's longer-run objective over the medium term.

The Committee

concluded that, although it had seen further progress, the economic conditions

warranting an increase in the target range for the federal funds rate had not

yet been met. Members generally agreed that additional information on the

outlook would be necessary before deciding to implement an increase in the

target range ...

And so, it seemed that

the Fed simply confirmed what everyone knew — that the economy was accelerating

— but not quite as fast as necessary to raise rates. At the end of the day,

markets were left "slightly lost, upset, and confused," as Deutsche

Bank's Jim Reid put it in a note to clients on Thursday. And this was enough to

squash expectations for September. The probability of a rate increase next

month plunged from 50% to 36% in a single afternoon on Wednesday.

And then, stocks

entered a correction

In two days, US stocks

tumbled far enough to log the worst week since September 2011. After falling to

a six-month low on Thursday, the Dow on Friday lost more than 500 points and

entered into a correction — defined as a 10% drop from recent highs. The

S&P 500 closed down 5% for the week and lost more than 100 points in a week

for the first time since 2008. On Friday afternoon, the probability for a rate

hike next month was lower still, at 34%.”

Corporate Earnings

True revenues and earnings are slowing somewhat but we do

not anticipate a severe earnings drought in the near-term. In our July

12th comments we wrote, “…it’s

also beneficial to look at the quality of earnings that are produced within the

S&P 500. I like to track the index net operating income less its cash flow

from operating and investing activities. One can then scale it by total index

assets for easier cross index comparisons but for simplicity the chart below is

shown as a z-score or where it lies on the bell curve. Knowing how much of

reported earnings is supported by cash received versus accrued is key when

using financial ratios and attaching a multiple to determine fair value.

When the earnings

quality line is falling, then earnings quality is deteriorating. When it’s

rising then it an earnings quality improvement. Notice both the market tops in

1999 - 2000 and 2007 – 2008 correlated with a -4 reading in the EQ chart. While

earnings quality currently is deteriorating, it is nowhere near the dangerous levels

of the previous two bear markets. For all the talk about sinister financial

engineering used to goose profits, it appears to me that there is still some

wiggle room to continue down this road for a while longer.”

Bottom Line: In the

near-term we are expecting the market to bounce from current depressed levels.

We will use this opportunity to book profits from our protective positions and

trade the bounce for our more opportunistic clients. Once the bounce has

happened we will reinstate the portfolio protection as we believe the market

will remain weak in the intermediate-term with a possible correction looming

(+10% from the peak). This could last through October. For the long-term we

believe this is a correction in a bull market and the economy and the market

will resume its uptrend. We will make portfolio adjustments as the data

dictates.

Joseph S. Kalinowski, CFA

Additional Reading

No part of

this report may be reproduced in any manner without the expressed written

permission of Squared Concept Partners, LLC.

Any information presented in this report is for informational purposes

only. All opinions expressed in this

report are subject to change without notice.

Squared Concept Partners, LLC is an independent asset management and

consulting company. These entities may have had in the past or may have in the

present or future long or short positions, or own options on the companies

discussed. In some cases, these positions

may have been established prior to the writing of the particular report.

The above

information should not be construed as a solicitation to buy or sell the

securities discussed herein. The

publisher of this report cannot verify the accuracy of this information. The owners of Squared Concept Partners, LLC

and its affiliated companies may also be conducting trades based on the firm’s

research ideas. They also may hold positions

contrary to the ideas presented in the research as market conditions may warrant.

This analysis

should not be considered investment advice and may not be suitable for the

readers’ portfolio. This analysis has been written without consideration to the

readers’ risk and return profile nor has the readers’ liquidity needs, time

horizon, tax circumstances or unique preferences been taken into account. Any

purchase or sale activity in any securities or other instrument should be based

upon the readers’ own analysis and conclusions. Past performance is not

indicative of future results.