The market is hitting new highs but we’re still waiting for

a better entry point to deploy new capital. We anticipate a pull-back in the

market that will offer itself as a buying opportunity. We believe it will be a

minor correction and not the start of something worse for several reasons.

The Pullback

The reflation trade is ongoing but needs to take a breather

in our opinion. Looking at sector performance over the past 100 days we can

clearly see the rally was led by cyclicals tied to an expected economic pickup.

Industrials, Materials and Financials have taken the leadership mantle.

That said, over the past several weeks we have seen

improvement in economically defensive sectors such as health care, consumer

staples and utilities. We anticipate this rotation can have a negative impact

on equity performance in the short-term.

This rotation is seen in our economically cyclical vs.

defensive index.

Short-term Yield

Analysis is worrisome

In addition to the sector rotation trends we have seen,

interest rate yield spreads are a reason to raise an eyebrow currently.

The first chart below compares the Moody’s AAA Investment

Grade Bond yield relative to the twelve month-forward earnings yield for the

S&P 500. This spread should move in the same direction as the stock market

to confirm a rally. What we are seeing now is the S&P 500 hitting new highs

while the IG/SPX yield spread is hitting resistance. The previous two times

this resistance was reached the stock market went into a brief correction. The

first time was very minor (approximately 6% from peak to trough) and the second

time the S&P 500 dropped roughly 12%.

When comparing the spread between investment grade and high

yield bonds, we can see that we are entering a range on the chart that is

usually indicative of some market turbulence on the horizon.

The relative price performance comparison between the

investment grade ETF (AGG) and the high yield ETF (HYG) is a good test to

confirm a market rally. While the trend between the two is down, we are looking

for hints of a small reversal. The AGG:HYG price ratio is the lowest it has

been in the history of these two ETF’s. We are looking for a reversal that

could impact the market in the short-term.

Lastly, we look at the Moody’s High Yield Bond rate relative

to the twelve month-forward E/Y for the S&P 500. This ratio should be

moving in the same direction as the overall market (SPX). Instead what we are

seeing is a major divergence between the two. As the stock market is hitting

new highs, the HY:SPX yield spread is moving in the opposite direction. This is

not a great sign for the strength of the current rally. Adds fuel to our thesis

on a short-term pullback.

On the technical side, we are approaching the top of the

upward channel but most market internals just aren’t confirming the market

rally. RSI and Stochastics are making lower highs as the market is making

higher highs. Volume on the days the market is rallying is soft and MACD

momentum is still sloping downward despite a bullish cross last week. The

percent of companies in the SPX in bullish P&F formations is making lower

lows as is the percent of companies in the SPX trading above their 50-day moving

averages. New Highs to New Lows are not confirming the rally nor is the comparison

of the SPX to the S&P 500 equal weight index.

All told we will not be crazy enough to short into this

market but we are waiting patiently to deploy new investment money if a pullback

were to happen. We are confident that a pullback would be quick and shallow in

nature and believe the overall bull market will remain in place at least

through the end of the year.

Coming Bear Market?

Not yet.

The Federal Reserve Bank of Atlanta publishes their GDP-Based

Recession Indicator Index. The latest reading shows a 5.3% chance of a US

economic recession on the horizon. The model is trending lower confirming an

economic expansion. A reading between 50% and 65% is usually a signal to start worrying

about.

Similarly the Federal Reserve Bank of St. Louis releases

their Smoothed U.S.

Recession Probabilities. They define the index as, “Smoothed recession probabilities for the United States are obtained

from a dynamic-factor markov-switching model applied to four monthly coincident

variables: non-farm payroll employment, the index of industrial production,

real personal income excluding transfer payments, and real manufacturing and

trade sales.”

They place the probability of a coming recession at just

under 3%.

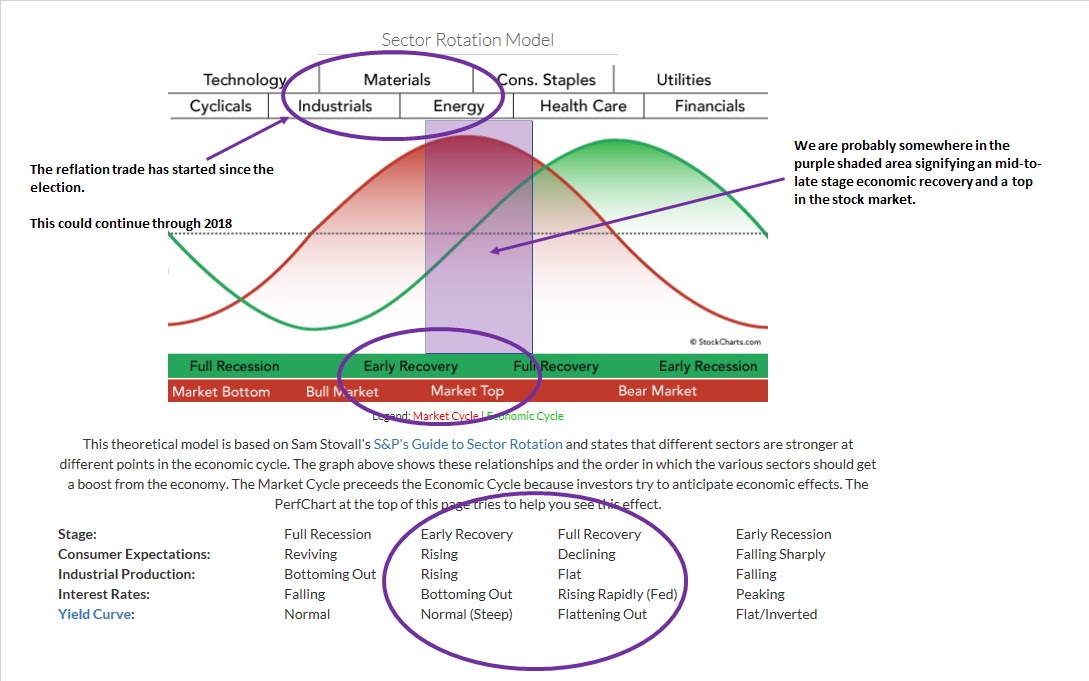

That said we do believe we are in the very late stages of

the economic cycle and thus the market cycle. As the figure below shows we

could get new market highs from the reflation trade as Materials, Industrials

and Energy lead the pack. This final cycle could very well last into 2018 but

at some point, the market cycle will turn.

We track the yield spreads between the two-year and ten-year

sovereign debt spreads across the globe. We break it down in three categories;

North American developed markets, European developed markets and Asia-Pacific

developed markets. We then weight each country’s yield curve by their GDP contribution

to the region. Since the US election, global yield curves have been steepening.

We believe this ties into our thesis of the reflation trade and higher stock

prices this year (see our blog post Investment Thesis for 2017).

The following three charts are the regional yield curves

weighted by each country’s GDP contribution to the region.

As the reflation trade ensues and global economic growth

starts to pick-up, he Fed and other world banks will need to start raising

short-term rates to keep inflation subdued. The market anticipates this action

and the market sells off. As the chart below shows, the beginning of a steepening

yield curve is a good thing for the stock market. During the steepening yield

curve process the market goes on to rally twelve to eighteen months after the

start of the steepening cycle.

Global yield curves have started steepening and the stock

market has started to rally on expectations of pro-growth, simulative policies

that could spur economic growth. Should these expectations become reality then

the yield curve steepening cycle should continue and the stock market could see

another twelve to eighteen months of gains.

The one difference this time around is that the US yield

curve never was inverted. It did come close but the use of unorthodox monetary

policy measures (Quantitative Easing and Operation Twist) after the Great

Recession could have skewed the results.

The primary reason for the market corrections are due to Fed

policy and their mandate to fight the effects of inflation and keeping a stable

currency. As the Fed starts to tighten in the later stages of the economic

growth cycle, this starts a new flattening cycle but by then the damage is

already done for equity investors.

One key variable to watch over the next year is inflation

expectations. With the reflation trade in full swing, it would make sense for

inflation expectations to become more elevated than in recent years past. This

would confirm the onset of a possible bear market in the future.

Tracking the spread between the 10Y TIPS and the 10Y US

Treasury yield is a way to look for potential problems.

Another tool to use in watching credit spreads is the LEI

Leading Credit Index. From the Conference

Board website, “This index is

consisted of six financial indicators: 2-years Swap Spread (real time), LIBOR 3

month less 3 month Treasury-Bill yield spread (real time), Debit balances at margin

account at broker dealer (monthly), AAII Investors Sentiment Bullish (%)

less Bearish (%) (weekly), Senior Loan Officers C&I loan survey – Bank

tightening Credit to Large and Medium Firms (quarterly), and Security

Repurchases (quarterly) from the Total Finance-Liabilities section of Federal

Reserve’s flow of fund report. Because of these financial indicators' forward

looking content, LCI leads economic activities.”

A sharp rise in the year-over-year growth figure for this

index usually represents tough economic times ahead. When this index starts

showing 10% y-o-y acceleration, it’s usually time to start protecting your

portfolio.

Bottom Line: We

believe short-term yield analysis is confirming our thoughts of a near-term

brief and shallow pullback. We will use this opportunity to deploy new assets

as we believe the reflation trade and steepening yield curve offers additional

upside to the market this year. We will be watching our yield spreads for

further confirmation or rejection of our thesis.

Joseph S. Kalinowski, CFA

Email: joe@squaredconcept.net

Twitter: @jskalinowski

Facebook: https://www.facebook.com/JoeKalinowskiCFA/

Blog: http://squaredconcept.blogspot.com/

No part of this report may be reproduced in any manner

without the expressed written permission of Squared Concept Asset Management,

LLC. Any information presented in this report is for informational

purposes only. All opinions expressed in this report are subject to

change without notice. Squared Concept Asset Management, LLC is a

Registered Investment Advisory and consulting company. These entities may have

had in the past or may have in the present or future long or short positions,

or own options on the companies discussed. In some cases, these positions

may have been established prior to the writing of the report.

The above information should not be construed as a

solicitation to buy or sell the securities discussed herein. The

publisher of this report cannot verify the accuracy of this information.

The owners of Squared Concept Asset Management, LLC and its affiliated

companies may also be conducting trades based on the firm’s research

ideas. They also may hold positions contrary to the ideas presented in

the research as market conditions may warrant. This analysis should not be considered investment advice and may not be suitable for the readers’ portfolio. This analysis has been written without consideration to the readers’ risk and return profile nor has the readers’ liquidity needs, time horizon, tax circumstances or unique preferences been considered. Any purchase or sale activity in any securities or other instrument should be based upon the readers’ own analysis and conclusions. Past performance is not indicative of future results.

No comments:

Post a Comment