I came across an article from the Washington

Post regarding President Trump’s comments on Russian President Vladimir

Putin. The article talks about President Trump’s upcoming interview tonight

with Fox News Bill O’Reilly. They quote,

“In an interview with Fox News's Bill

O'Reilly, which will air ahead of the Super Bowl on Sunday, Trump doubled down

on his “respect” for Putin — even in the face of accusations that Putin and his

associates have murdered journalists and dissidents in Russia.

“I do respect him.

Well, I respect a lot of people, but that doesn’t mean I’ll get along with

them,” Trump told O'Reilly.

O'Reilly pressed on,

declaring to the president that “Putin is a killer.”

Unfazed, Trump didn't

back away, but rather compared Putin's reputation for extrajudicial killings

with the United States'.

“There are a lot of

killers. We have a lot of killers,” Trump said. “Well, you think our country is

so innocent?””

I suppose comments like that is the draw of many Americans

that have supported his rise to the most powerful position in the world. Nevertheless,

it reflects his shoot from the hip approach towards elaborating on his policies

that could pose problems in the future, specifically as it relates to the

equity and capital markets.

Further, his mixed message on border taxes has raised several

questions. From Business

Insider, “Everyone seems to be

talking about a border tax these days — but few people seem to know what

they’re talking about.

One reason is the

neophyte US president’s own mixed message. As he has done on multiple

occasions, President Trump has taken both sides of this particular issue at

various times.

On January 16, Trump

said he was hesitant to impose a border tax on imported goods as part of his

anti-trade push: “Anytime I hear border adjustment, I don't love it,” he

said at the time. It’s “too complicated,” Trump added.

Days later, the

president had changed his mind. "If you go to another country and you

decide that you're going to close and get rid of 2,000 people or 5,000 people

... we are going to be imposing a very major border tax on the product when it

comes in," Trump warned during a meeting with CEOs.”

Additional taxes and tariffs with the potential to start

trade wars is not perceived as a pro-growth benefit for the economy or the

stock market.

In our opinion it just may be a matter of time before

President Trump turns his twitter rants towards a stock market that he himself

deemed a bubble. Jesse Felder from The Felder

Report summed it up nicely, “With

economic optimism soaring since the election, rising risks to the economy and

financial markets have fallen off Mr. Market’s radar. However, there are a

number of reasons to believe Donald Trump and his advisers are well aware of

these risks and have already made plans to address them sooner rather than

later.

To this point, Mark

Spitznagel recently wrote, “The ‘big, fat, ugly bubble’ in the stock

market that President-elect Donald J. Trump so astutely identified

during his campaign now becomes one of the greatest potential liabilities of

his presidency.” From a political standpoint, the sooner Trump and his

administration deal with these risks the easier it will be to blame on the

prior administration. Allowing them to fester for any period of time increases

the likelihood they will take the blame for the bubble’s bursting.”

“Interestingly, Trump

recently named Carl Icahn as a special advisor to his new administration. You

may remember that Icahn recently warned of “Danger Ahead” for risk markets:

“I’ve seem this before

a number of times. I been around a long time and I saw it ’69, ’74, ’79, ’87

and then 2000 wasn’t pretty. A time is coming that might make some of those

times look pretty good… The public, they got screwed in ’08. They’re gonna get

screwed again. I think it was Santayana that said, “those who do not learn from

history are doomed to repeat it,” and I am afraid we’re going down that road.”

So Trump is clearly

not running away from his famous “big, fat, ugly bubble” comment. Just the

opposite. In fact, it was probably Icahn who helped him to fully appreciate

just how dangerous the current situation is. In naming Icahn to his special

advisory position he is demonstrating that he takes the risks currently posed

by the financial markets very seriously.

In a

recent interview on CNBC, Icahn echoed his concerns once again:

Most telling is how

Icahn ended the interview, unprompted. “If you’re asking me am I concerned

about the market on the short term. Yeah I’m concerned about it,” he said. “You

can look at so many factors here that you have to worry about. Obviously, if

you get into a trade war with China, sooner or later, I think we’re going to

have to come to grips with that, maybe it’s better to do it sooner…”

It sounds like Icahn

may be counseling the president that it’s in everyone’s best interest to deal

with the glaring “dangers” posed by the financial markets to both the economy

and to Trump’s presidency “sooner” rather than later. For these reasons, I

wouldn’t be surprised to see the administration make, in Spitznagels words,

‘encouraging asset prices and investments to correct themselves,’

its first order of business after the inauguration today.”

Rubber Meets the Road

We have commented in past writings that “animal spirts” and

market sentiment has skyrocketed since the election. That said, there is going

to come a time where actions need to justify the rhetoric. Take Fridays jobs

report for instance. The headline number appears very strong and Donald Trump

was very quick to take credit for and hype the figure. He was quoted as

praising the headline figure saying, “227,000

jobs, great spirit in the country right now, I think it's going to continue,

big league.”

Yet during the campaign he was much more pessimistic towards

how the unemployment figures were calculated. Quoting from The

New York Times, “But Mr. Trump made

amply clear in his campaign that he doesn’t care for the way that government

agencies and mainstream economists summarize the state of the job market. The

unemployment rate, he said in December, is “totally fiction.” He claimed at one

point during the campaign that the real jobless rate was not the number below 5

percent widely cited by economists, but something like 42 percent.”

I know…I know…the New York Times and President Trump are at

war. That said it is quite clear that Mr. Trump was bashing the conclusions of

the survey not that long ago, except when the headline number confirmed his

bias. Regardless of the fact that much of this report was conducted while

President Obama still held office and a deeper look at the numbers wasn’t all

that impressive, Mr. Trump still went out of his way to praise the survey

results.

According to Business

Insider, “The release from the Bureau

of Labor Statistics showed that the US economy added 227,000 jobs in the month

of January. Wage growth disappointed, however, and the unemployment rate ticked

up slightly to 4.8%.”

Scott Grannis of Calafia

Beach Pundit went further in his analysis. He writes, “Job gains in January beat expectations by a significant margin (+227K

vs. +180K), but from a big-picture perspective, nothing much has changed

over the past six months or so. Private sector jobs (the ones that really

count) are growing at a modest 1.8% rate, the rate which has prevailed since

last summer. We've seen an uptick in animal spirits (e.g., consumer confidence,

small business optimism, equity prices), but it hasn't yet translated into

anything substantial on the employment front.”

“As the chart above

shows, monthly changes in private sector jobs can be, and typically are, quite

volatile. You can't draw strong inferences from one month's numbers.”

“The chart above looks

at the rate of change in private sector jobs over the past six and twelve

months. This has been roughly 1.8% since last summer, and that is a relatively

slow pace even for this relatively tepid recovery. We'd have to see a few more

months of job gains like January's before getting excited. I'm not saying this

won't happen, just that it's premature to declare that the pace of economic

growth has accelerated.”

There has come a time where the actual economic figures

lives up to the hype that is currently baked into the market valuation. Lance

Roberts of Real

Investment Advice pointed out the dichotomy between expectations and

reality. He comments, “We can see this

more real time by looking at the Chicago Fed National Activity Index (CFNAI)

which is arguably one of the more important economic indicators. The index

is a composite made up of 85 subcomponents which give a broad overview of

overall economic activity in the U.S. However, unlike backward-looking

statistics like GDP, the CFNAI is a forward-looking metric that gives some

indication of how the economy is likely to look in the coming months.

Importantly, understanding the message the index is designed to deliver

is critical. From the Chicago Fed website:

“The Chicago Fed

National Activity Index (CFNAI) is a monthly index designed to gauge overall

economic activity and related inflationary pressure. A zero value for the

index indicates that the national economy is expanding at its historical trend

rate of growth; negative values indicate below-average growth, and positive

values indicate above-average growth. “

The overall index is

broken down into four major sub-categories which cover:

Production &

Income

Employment,

Unemployment & Hours

Personal Consumption

& Housing

Sales, Orders &

Inventories

Here is my point.

While “exuberance” in terms of “attitudes” is surging, actual activity remains

quite subdued. The first chart compares my combined consumer confidence composite

to the CFNAI.”

“The next chart is the

dispersion of the components of the CFNAI also compared to consumer

“confidence.””

“In both instances

there is a wide deviation between “attitude” and “activity.” More importantly, “attitudes” have

typically reverted back to “activity” rather than the other way around.

This potentially

leaves the market set up for disappointment in the months ahead. Be careful.”

In our previous blog post, Investment Thesis for 2017 we wrote, “We believe that the US equity markets are

chugging higher more on investor sentiment than underlying fundamentals. Should

we get confirmation that expectations are becoming a reality then we could see

the next leg higher in the stock market. This will most likely happen as the

economy experiences a “sugar high” from continually accommodative monetary

policy and a burst of fiscal stimulus.”

We certainly understand the underlying risks to our bullish

2017 investment thesis rides on market perception becoming a reality.

Hints of Skepticism

We’re coming across reports that are starting to doubt

President Trumps ability to live up to the fanfare surrounding his election.

This stems from the campaign promises of fiscal stimulus, deregulation and tax

reform. All of these measures are considered pro-growth policies as judged by

the market reaction but thus far into his presidency he has decided to tackle

the more controversial issues. Namely his policy stance on trade has many nervous

about the direction that his administration is likely to take.

From Business

Insider, “So far Deutsche Bank has

been horribly wrong about the "defining feature of Trump's economic

approach." It hasn't been deregulation and an "expansionary fiscal

policy" (fancy words for stimulus); it has been trade (or rather

opposition to it).

And, everything Trump

said about trade on the campaign trail — which he is now forcing us all to take

quite literally — happens to be terrible for business. Deutsche Bank gave this

a passing acknowledgment in its note, saying simply: "Uncertainty about

the Trump administration's policies is still large, as is the reaction of those

impacted by these policies."

Well now we know more

about the policies and we know more about the reactions. Neither has been

great. Trump wants to rip up bilateral trade deals and renegotiate them one by

one.

In an interview with

Business Insider, trade policy expert and Carnegie Mellon economics professor

Lee Branstetter told us this may not be the best idea.

"That is an

incredibly expensive time-consuming way to recreate what you already

have," he said.

Last week Trump

described how he'd be doing that: basically handing countries a list of

demands, giving them 30 days to respond, and then, if they do not comply, hitting

them with tariffs. Making demands is an excellent way to upset a country, as we

learned last week when Mexican President Enrique Peña Nieto canceled a meeting

with Trump after Trump demanded in a badly timed tweet that Mexico pay for a

wall along the US's southern border.

This is the kind of

manic communication that insults nations and starts trade wars. If Trump keeps

insulting countries like Mexico and China, they can retaliate and put thousands

of American jobs at risk.

Branstetter told us

that if you know anything about the Chinese, you should know they're ready to

retaliate if they feel as if they've been hit first. Hit doesn't even mean only

economically. In an interview with NBC, China's Foreign Ministry spokesman said

the US's One China policy — the recognition that Taiwan is a part of China —

was not up for debate. Violating that would be grounds for retaliation, and

Trump has already tested it by taking a call from the president of Taiwan.”

Expectational

Exuberance?

Will it be possible for President Trump to live up the

expectational exuberance that has entered the mindset of market participants?

In the Pragmatic

Capitalism blog writings, they state, “When

Obama was coming into office the public was so euphoric about change that the

approval numbers were unsustainably high. At the same time, the cyclical trend

in the economy was so bad that there was a high probability of some mean

reversion and recovery. The public’s overall sentiment was better captured in

President Bush’s low approval rating of 35% at the end of his second term and

the consumer confidence figures which bottomed in 2009. In other words,

President Obama was becoming President at an extremely fortunate time. And

although he probably underperformed his stratospheric expectations he did

better than most probably expected.

And here’s the

interesting part about Trump’s Presidency – how much room is left in this

balloon? For instance, how much higher can consumer confidence go?”

“Or, how much more

employment can you pull out of an economy plumbing very low levels of

unemployment?”

“This looks like a

balloon that is much closer to its max capacity than vice versa. And while I

certainly think there’s room to grow you have to wonder if we aren’t seeing the

exact opposite reaction to Trump that we saw to Obama. In other words, are

Trump’s approval figures too low and are his expectations for economic growth

unrealistically high? I don’t know the answer and I certainly don’t know

the timing of the end of economic cycles, but this balloon looks a lot closer

to full expansion than the economy that Barack Obama inherited. And so the

smart betting man to has think that the potential for greater instability is

higher today than the economy that was so unstable at the start of Barack

Obama’s term.”

Perhaps a better analogy is a comparison to market activity

at the onset of President Reagan. Similar to the start of President Obama’s

first term, economic conditions at the start of President Reagan’s first term

surely was starting from a bar that was set much lower.

From the AB

blog, “Investors excited by the boost

the US election gave to US stocks should recall that starting conditions

matter. This is not 1981, the beginning of the Reagan era.

When Ronald Reagan

took office 36 years ago, the US economy was in a deep recession induced by

extremely high interest rates intended to wring out inflation. Back then, the

S&P 500 was trading at around nine times depressed forward earnings, as the

Display below shows.

When Donald Trump took

office, the S&P 500 was trading at about 18 times forward earnings—and

earnings were close to all-time highs. Yet, the fed funds rate was around 0.5%,

and the 10-year Treasury rate, about 2.5%. While both interest rates are higher

than a few months ago, they remain close to all-time lows, and are poised to go

higher.”

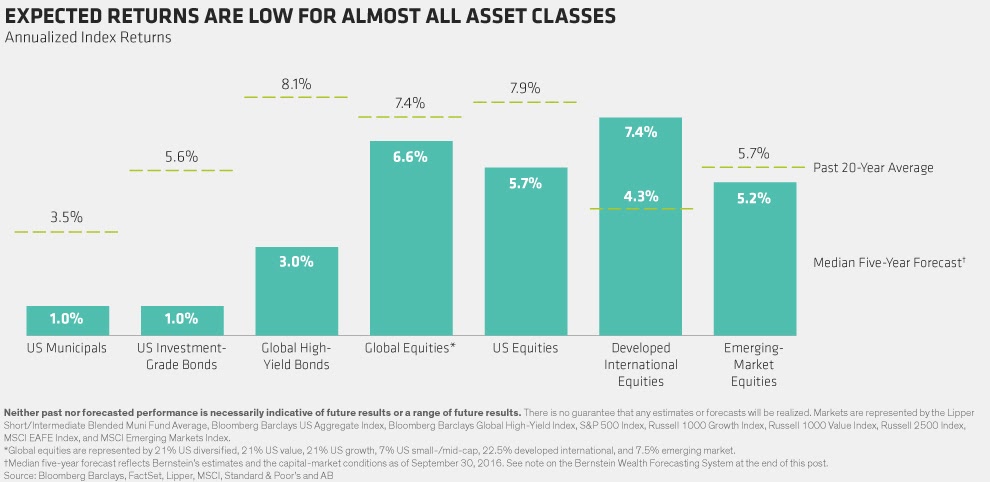

The folks at Alliance Bernstein are not expecting capital

market returns to be anywhere near the returns found in the Reagan or Obama

first term presidencies.

“Stock returns are

also likely to be subpar: Our central case calls for US stock market returns of

less than 6% annually over the next five years, below their nearly 8% average

over the past two decades. Even if the new administration and Congress agree on

policies that boost GDP growth and extend the economic cycle, earnings growth

is likely to be limited and much slower than in the early years of the recovery.

Why? Profit margins are close to record highs and could be hurt by

protectionist trade policies.

A reduction in US

corporate tax rates could add to after-tax earnings for some companies,

however. This is an area where research-based stock selection will be critical.

Overall, we expect modest gains from earnings growth and dividends to be

somewhat offset by valuation contraction.”

This past week John Hussman of Hussman Funds

lambasted President Trump, albeit in a cordial and polite way. “From my perspective, the problem isn’t

politics. A civil society can work out those differences. The immediate

problem, and the danger, is the mode of leadership itself. A leader can call

forth either the “better angels of our nature” or the worst ones. I am troubled

for our nation and for the world because of the example of coarse incivility,

mean-spirited treatment of others, disingenuous speech, thin temperament,

self-aggrandizing vanity, puerile character, overbearing arrogance, habitual

provocation, and broad disrespect toward other nations, races, and religions

that is now on display as our country’s model of leadership. Despotism reveals

itself through a reliance on threat, intimidation, bullying, coercion, and a

chilling instinct to address problems through forms of termination, such as the

killing of enemies and the exclusion and dismissal of adversaries. I am equally

troubled by emerging risk, discussed below, to the Constitutional separation of

powers.”

He goes on to write about potentially misguided policies and

how these policies would negatively impact an already overvalued stock market

and a lackluster economy. “While

references for many of the foregoing observations are easily available, the

basis for a few of the economic and financial comments is provided below. For

data and evidence regarding labor market demographics and the components of GDP

growth, see my December 12, 2016 comment Economic Fancies and Basic Arithmetic.

On the relationship

between the trade deficit and U.S. gross domestic investment, the following

chart shows data since 1947, and captures the inverse relationship. Think of it

this way: Whenever we import a dollar of goods and services, we export a dollar

of “stuff” in return. That “stuff” can either be goods and services, or

securities. So by definition, when the U.S. is a net exporter of securities to

foreign investors, it must also be running a trade deficit in goods and

services. That’s just an accounting identity.

Investment and savings

must be equal in equilibrium (this is also an accounting identity). From a

financial perspective, an export of U.S. securities is an import of foreign

savings. Putting this all together, booms in U.S. gross domestic investment

(factories, capital goods, equipment, housing) are typically financed by an

import of foreign savings and corresponding “deterioration” in the trade

deficit. Conversely, “improvement” in the trade deficit is systematically

related to deterioration in U.S. gross domestic investment.”

“The result of all

this is that U.S. investment booms are typically associated with a widening,

not a narrowing, of the U.S. trade deficit. If you really want a collapse in

U.S. gross domestic investment, cannibalize national savings by expanding the

U.S. budget deficit through massive spending projects and lower taxes, and simultaneously

limit the import of foreign saving by provoking a trade war aimed at

“improving” the U.S. trade deficit. That’s precisely the direction this

administration is heading. It seems we’ve forgotten the consequences of the

Smoot-Hawley Tariff, which was passed in June 1930, at the outset of the Great

Depression.”

“To offer a sense of

what’s likely to unfold, the following chart shows the ratio of nonfinancial

market capitalization to corporate gross value added (MarketCap/GVA), which is

more strongly correlated with actual subsequent S&P 500 total returns than

any alternative measure we’ve studied over time. In the chart below,

MarketCap/GVA is shown on an inverted log scale in blue. The red line is the

actual subsequent S&P 500 nominal total return over the following 12-year

period. At present, we project a likely market loss over the coming decade,

with S&P 500 total returns averaging just 1% annually over the coming 12

years. Those aren't much different than the awful market outcomes I projected

in real-time at the 2000 market peak. In that instance, the S&P 500 lost

half of its value over the completion of the market cycle, with negative total

returns for a buy-and-hold approach from March 2000 all the way out to November

2011. Every investment strategy has its season. My sense is that passive,

value-insensitive investors are now facing another long, hard winter.

Meanwhile, flexible, value-conscious investors are approaching the first day of

spring.”

“The following chart

shows some of the most reliable valuation measures we identify in terms of

their percentage deviations from historical norms. These measures are currently

125% to 150% above (2.25 to 2.50 times) norms that have regularly been

approached or breached over the completion of market cycles across history. At

the 2000 and 2007 peaks, we correctly projected the probable extent of the

losses that passive investors faced over the completion of the market cycle.

Presently, we estimate that this speculative cycle will be completed by market

loss in the S&P 500 in the range of 50-60%.

Bottom Line: Our

bullish call for 2017 makes several assumptions about monetary and fiscal

policy, economic growth and corporate profits. While valuations are certainly stretched

by historical standards, we understand that the stock market can be driven for

months and years by extreme levels of euphoric sentiment. We believe this to be

the case today.

We believe there

exists one more leg higher that could be called the “blow-off top” before

underlying market fundamentals start to drive prices lower.

The risk to our

thesis is a sudden deceleration in economic fortunes but more importantly a

negative change in sentiment from this point.

Joseph S. Kalinowski, CFA

Email: joe@squaredconcept.net

Twitter: @jskalinowski

Facebook: https://www.facebook.com/JoeKalinowskiCFA/

Blog: http://squaredconcept.blogspot.com/

No part of this report may be reproduced in any manner

without the expressed written permission of Squared Concept Asset Management,

LLC. Any information presented in this report is for informational

purposes only. All opinions expressed in this report are subject to

change without notice. Squared Concept Asset Management, LLC is a

Registered Investment Advisory and consulting company. These entities may have

had in the past or may have in the present or future long or short positions,

or own options on the companies discussed. In some cases, these positions

may have been established prior to the writing of the report.

The above information should not be construed as a

solicitation to buy or sell the securities discussed herein. The

publisher of this report cannot verify the accuracy of this information.

The owners of Squared Concept Asset Management, LLC and its affiliated

companies may also be conducting trades based on the firm’s research

ideas. They also may hold positions contrary to the ideas presented in

the research as market conditions may warrant.

This analysis should not be considered investment advice and

may not be suitable for the readers’ portfolio. This analysis has been written

without consideration to the readers’ risk and return profile nor has the

readers’ liquidity needs, time horizon, tax circumstances or unique preferences

been considered. Any purchase or sale activity in any securities or other

instrument should be based upon the readers’ own analysis and conclusions. Past

performance is not indicative of future results.