For the most part we have spent 2016 on the short side of

the market. On Friday we decided to take off all of our short positions in our

trading account and are waiting for signs of a follow-through of Friday’s rally

to take a long position once again. We were a bit surprised that the market

retained its gains heading into a three day weekend but the market proved

resilient, albeit on low volume. News on the oil front about production

controls has the market in full risk-on mode this morning. Here are a couple of

near term items that lends itself to a rally from here.

Item #1: The

economic picture has improved slightly putting into question the worries of a

U.S. economic recession. From Business

Insider, “Retail sales jumped more

than expected in January, up 0.2%.

Excluding autos and

gas, the advance estimate from the Census Bureau showed that retail sales rose

0.4% compared to December. And, the retail sales control group, which feeds

into GDP calculations, rose 0.6%.”

Consumer sentiment remains relatively stable as well. “Over the last few weeks, concerns had

mounted that the recent market turmoil would soon dampen consumer confidence

and spending.

But consumer sentiment

remains at a relatively elevated level, even after the unexpected drop in the

University of Michigan's index to 90.7. And as TD Securities' David Tulk argued

in a note to clients, it's still too soon to tell whether the sell-off in stocks

will be followed by an economic downturn.

A downturn in stocks

can be a leading indicator of economic activity but doesn't serve as one on a

consistent basis.” (Business Insider).

This is positive news in the face of deteriorating stock

returns and the negative wealth effects it can have on the consumer. One

possible explanation comes from Deutsche

Bank's Torsten Sløk. He states (via Business

Insider), “Many are worried about

what the hemorrhaging stock market could mean going forward for the overall

economy.

But Deutsche Bank's

Torsten Sløk argues that the negative wealth effect on the economy caused by

investors freaking out about turbulence in the markets shouldn't be too huge

because middle income consumers are feeling good.

In a recent note to

clients Sløk wrote that, generally speaking, an increase in wealth has a

greater impact on consumer behavior than a decline in wealth.

"Given how small

the positive wealth effects have been over the past seven years then it would

be a surprise if the negative wealth effects are big, in particular in a

situation with consumer sentiment for middle income groups rising in January

and at levels higher than in 2005 — 2006," he argued.

"Put differently,

the lack of a slowdown in the broader macro data including consumer sentiment,

the unemployment rate, the quits rate, job openings, hours worked, wage inflation,

and jobless claims [Thursday] morning, suggests that the negative wealth

effects are indeed going to be limited," he continued.”

Additional information from XE

blog also shows things may not be as bad as feared on the economic front.

They state, “Recent

market and statistical weakness has led to increased discussion of a possible

US recession. In this column, I will

argue that instead of a recession, we’re facing a situation similar to the

mid-1980s, where the economy also experienced slowdown caused by high oil

prices, a strong dollar slowdown and weak oil sector. But there is insufficient weakness – largely

thanks to continued housing market strength and recent wage growth – for a

recession to occur.”

When looking at the quarter over quarter economic growth

figures, “Between 1Q15-4Q15, personal

consumption expenditures (PCEs) fluctuated between .6% and 3.9% Q/Q

growth. Durable goods purchases varied

between 2%-8% growth – an encouraging pace.

And service spending was constant, with numbers seesawing between

2%-2.7%. Investment is where problems

emerge. Non-residential structural

spending contracted in 3 of the last 4 quarters; spending on equipment was weak

in 2Q14 (.3% increase) and contracted in 4Q15.

But residential investment grew strongly in all four quarters. And finally, we have exports, which

contracted in 2 of the last four quarters.

The Q/Q numbers show modest growth, with the weak oil/gas extraction

market and strong dollar hurting growth.”

Using the same metrics and analyzing year over year figures

they write, “Topline PCE growth recorded

levels between 2.6%-3.3% for the last 4 quarters – a decent pace of

growth. Consumer durable goods

expenditures were very strong, vacillating between 5.2% and 7.3%. As with the Q/Q figures, Y/Y business

investment numbers were weak; non-residential structural investment declined in

3 of the last 4 quarters. But

residential spending increased at a solid pace.

And exports declined in the 2H15.

So, like the Q/Q numbers, we again see evidence of industrial and export

weakness.”

When speaking to leading and coincident economic indicators,

“The LEIs have printed either 0 or

negative readings in 4 of the last 7 months while the CEIs have printed between

.1 and .3 (top table). But while the

lower table shows a slowdown in the LEIs 6 month rate of change, the CEIs

increased. Here is the conclusion

reached by the Conference Board’s economists

The Conference Board

LEI for the U.S. declined in the final month of 2015, with its six-month growth

rate decelerating. In addition, the strengths among the leading indicators are

now balanced with the weaknesses. Meanwhile, the CEI has continued rising

slowly, and as a result its six-month growth rate is higher than in the first

half of 2015. Taken together, the current behavior of the composite indexes and

their components suggest that while risks to growth have increased, although

not significantly, the expansion in economic activity should continue at a

moderate pace in the near term.

In theory, LEI

weakness should translate into CEI weakness.

When that doesn’t happen, it is more likely than not that a recession

isn’t likely.

The reason for the

current slowdown is a combination of weak international growth, a strong dollar

and weak oil prices. The economy faced

the exact same set of facts in the mid-1980s.”

Item #2: There

has been heavy shorting of the stock market from hedge funds and at least in

the near term much of the negativity surrounding interest rates, oil prices,

corporate earnings, slowing global economic growth etc. may be reflected in

prices. Again we state that this is a near term phenomenon. We continue to

believe there exists the potential for the market to drop significantly lower

from these levels. That said, any bit of positive news (oil production, Fed

dovishness, additional QE from global central bankers) could spark a near term

rally that could start a short squeeze and higher equity prices.

Citing a story from ValueWalk, “Behavior at market lows is always

interesting, and the February 9 notes that $59 billion of net shorts that have

been added in S&P 500 futures over the past 30 trading days. Who has been

engaged in this selling? It is a key alternative investment category, among the

biggest users of futures, who got short recently.

“On our books over the

past two weeks, it has been Hedge Funds that have seen a significant shift

towards short positioning,” the Morgan Stanley report said. “The % of Hedge

Funds that were short S&P 500 futures as of Friday’s close was the greatest

it’s been since the week of September 11, 2015 and, prior to that week, since

the fall of 2011.”

In the relative value

camp, the report noted on Monday’s close, US Long/Short Net Leverage returned

to post-crisis lows. Looking from a different perspective, gross leverage

remains 14-15% above its ‘10/’11 troughs, the report noted.”

“On a short term

basis, Morgan Stanley’s “Pain Monitor,” measuring open interest, it touching a

historic mean reversion point. On a fundamental level, often times when a trend

ends market participants will have exhausted a significant directional capacity

to contribute to price persistence. In many cases this leads to a mean

reversion point.

Looking at the “Pain Monitor”

exposure level mean reversion opportunities appear to exist in other markets,

not just the S&P, setting up some interesting correlation trades.

David Rosenberg seems

to agree. In his latest note to client he states:

One last item to note

which is sentiment (that wonderful contrary indicator at extremes). The

Investor’s Intelligence survey just came out for the past week and the bull

camp retreated to a five-month low of 24.7% from 34%; and the bear share edged

up to 39.2% from 27.9%. So the bull/bear spread widened out to -11.1 from -4.1

which indeed is a step in the right direction for those seeking a near-term

tradeable rally at the very least. This takes out the -10.4 level hit last

summer and not far off the-11.9 reading reached in 2011 that presaged a nice

bounce back at the time as the shorts ran for cover. Remember, the large

positive spread in favor of the bulls (+43.5 in April) touched off this severe

corrective phase. What goes around comes around.

Indeed, the latest Commitment of Traders Report

shows there now to be an eye-popping 46,738 net short S&P 500 contracts on

the Chicago Mercantile Exchange … surging four-fold so far this year to the

highest level since late November, 2011.”

Item #3: The

transportation sector seems to be catching a bid. According to the latest Cass Freight Index Report, “The number of freight shipments and the

dollars spent on freight have been in a typical seasonal decline since

September 2015. Our shipment index opened the year just 0.2 percent below last

January, while the expenditures index is down 1.4 percent. The economy grew

much more slowly in the second half of 2015, so January freight shipments are

down 11.6 percent and dollars spent are down 11.5 percent from the June 2015

high. The declines in the fourth quarter and again in January are normal

seasonal trends and are not necessarily signs of further weakening.”

On shipment volumes, “Year

over year, freight shipments were essentially flat from last year, just 0.2

percent lower than last January. Sequentially, January was the fourth month in

a row that the number of freight shipments declined. The Association of

American Railroads (AAR) reported that carloads were down 20.6 percent, while intermodal

loadings fell 11.9 percent over December 2014. The AAR attributed the decline

to soft economic conditions in the U.S. and globally. The continued steep

decline in energy prices hurt the railroads on several fronts in January.

First, it caused a dramatic decline in coal shipments, one of their primary

commodities, as power generating plants continue to shift to less expensive

natural gas. Second, a drop in petroleum and petroleum products shipments as

oil mining came to a virtual standstill in the U.S. And third, there has been a

loss of shipments of materials used in petroleum extraction. Truck tonnage also

eroded in January, but not to the same extent as railroads. Carriers are

reporting that capacity and demand are very well matched right now.”

On freight expenditures, “The

freight payment index fell 1.9 percent in January (from December), and is 1.4

percent below the January figure in 2015. The decrease in January 2016 is much

less than the December to January drops of 5.7 percent in January 2015 and 5.1

percent in January 2014. The decrease can be mainly accounted for by the drop

in the number of shipments and the mix of commodities moved. Generally

speaking, rates were stable in January because available capacity was not a

problem.”

They go on to summarize, “The

Institute of Supply Management’s (ISM) monthly PMI Index Report in January

showed that although the PMI Index remained below the 50 percent

threshold—indicating that manufacturing is contracting—the index rose for the

first time in four months. The 0.4 percent increase is a sign that

manufacturing may be reawakening. The Production Sub-index rose 0.6 percent,

along with a healthy 5.5 percent increase in the New Order Sub-index. If

manufacturing continues to grow—and it should—freight levels will return.

Although factory employment has been hit hard by weak exports, job hires were

up 29,000 in January.

The Labor Department

released figures recently showing another decline in unemployment, which fell

to 4.9 percent. Even better news for the economy is that there was a half a

percentage point gain in average hourly earnings in January. This, coupled with

the growth of wages in the second half of 2015, should increase consumer

spending, giving the economy another boost. Wages have grown more in the last

six months than in any other time since the recovery began over six years ago.

The number of new jobs created in January was much lower than in December, but

much of this is due to the hiring of seasonal workers.”

It’s not quite a ringing endorsement on all things moving

but certainly not gloom and doom.

In fact the transportation industry could be on the verge of

a major bottom as pointed out in See

It Market. They write, “To give you

an idea, the Dow Jones Transports is down over 20 percent in the last 12

months, having fallen over 30 percent from the late 2014 highs to January 2016

lows.

Below is a chart

looking at the Dow Jones Transportation Average/S&P 500 ratio over the past

10 years. The ratio shows that the Dow Jones Transports has been much weaker

than other stock market averages over the last year.”

“After hitting channel

resistance at point (1) a year ago, the Dow Jones Transports declined nearly

declined as hard as it did during the 2009 collapse. This decline took the

Transports relative strength down to channel support at point (2), where a

small rally has now taken place off the January lows. This could simply be a

bounce, but it is reflecting some relative strength against the broader

markets… for the first time in a year.

Below looks at the Dow

Jones Transports Index As you can

plainly see, it has been a painful decline.

The decline over the

past year has taken the Dow Jones Transports from channel resistance back down

to its rising trend support at point (1). This major support level also happens

to be the 38 percent Fibonacci retracement level as well (of the 2009 lows/2015

highs). As the Dow Transports Average was hitting this confluence of support a

few weeks ago, it also created a reversal candlestick at point (1).”

A rebound in the transportation sector could act as

positive reinforcement for the greater markets that a recession isn’t likely

and this pullback should be considered a correction. At the very least it may

provide a brief short term tailwind for the markets.

Item #4: The

percent of companies in the S&P 500 that are in a bullish point and figure

formation are extremely low and are signifying the possibility of a near term bounce. Currently only 29.8% of the

companies in the S&P 500 are in bullish point and figure formations (and

this is after the rally on Friday, on Thursday the figure was 27.6%). Typically

when this figure falls below 30% it represents a near term bottom in the

market.

We have been tracking this data since the early 1990’s and

there have been a few occasions when this metric was this low. The good news is

that this is a strong indication that a tradable bottom is available in the

near term. The bad news is that once this signal is initially met, there is a

pattern of more to come and the market has usually gone lower from that point. In

a word this metric becomes active in pinpointing short term rallies in a down

trending market. It gave us several tradable rallies starting in late 4Q 1998,

3Q 2001, 2Q 2002 before finally bottoming in 1Q 2003. It also registered in 1Q

2008 for a tradable rally then giving us another reading in 1Q 2009. As one can

see from the start of the first tradable bounce to that last the market got

destroyed both times. Only in 3Q 2011 did the initial reading pick the bottom.

In 3Q 2015 we got our first reading for a tradable rally and

now this past week we got a reading for 1Q16. This may be the final reading in

this correction but given the technical damage to the market it’s hard to

imagine the lows have been set.

Item #5: There

appears to be bullish divergences all over the daily chart for the S&P 500.

All the oscillators that we track are oversold and exhibiting a bullish

divergence. The MACD, percent in bullish point and figure formation, percent

of companies above their 50 and 200 day moving average and percent new hi/lo all exhibiting

a bullish divergence. This adds to the trading thesis that we are expecting a

near term bounce in the market. On the weekly chart all measures are oversold.

We believe that if the rally from the daily metrics are strong enough to spark

and improvement in the weekly metrics, we could see a sharp rally into the end

of 1Q16 and into 2Q16.

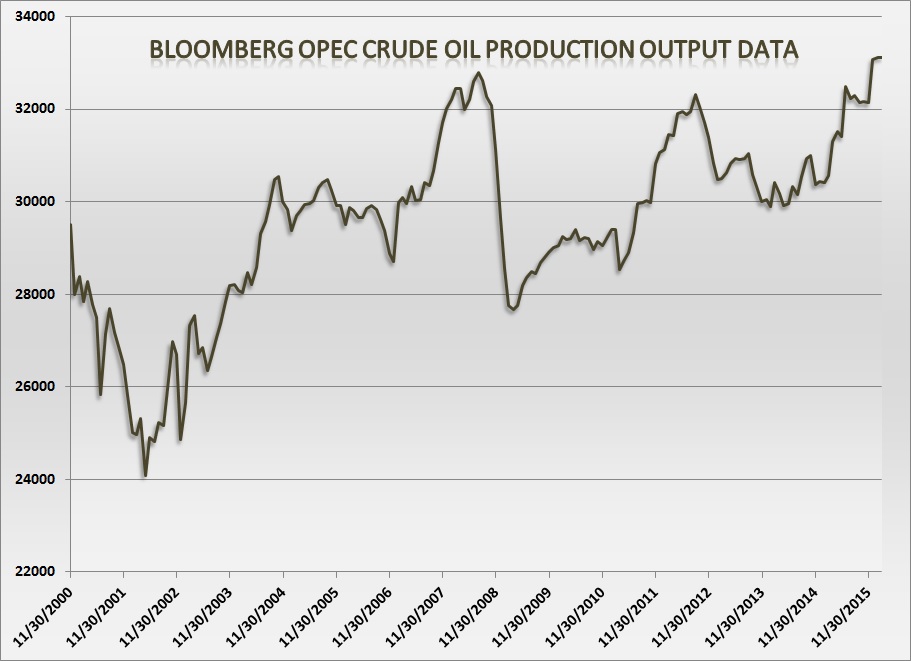

Item #6: Oil

prices have stabilized. This news is breaking as I write this analysis. According

to a note I just received from Seeking

Alpha, Russia, Saudi Arabia agree to

freeze oil output.

They summarize:

“Top oil officials

from Russia, Saudi Arabia and several key OPEC members have agreed to freeze

crude output at January levels at a meeting in the Qatari capital Doha,

targeting a supply glut that's sent prices to 13-year-lows.

According the

International Energy Agency, Saudi Arabia produced 10.2M bpd last month, below

its most recent peak of 10.5M bpd set in June 2015. Russia produced nearly

10.9M bpd in the same month, a post-Soviet record.

Oil soared almost 6%

ahead of the meeting - on expectations of a more weighty announcement - but

pared gains following the news. Crude futures +1% to $29.72/bbl.”

We think this could prove a nice tail wind for the market in

the near term as the correlation between oil prices and equity prices have been

higher than normal recently. The next chart found in an article entitled Oil Is the Cheap Date From Hell found in

BloombergBusiness

shows that correlation.

The article states, “History

is a useful guide. So far this year, the S&P 500 is moving in closer tandem

with West Texas Intermediate, the benchmark U.S. crude oil, than in any year

since 2000 except for 2010. The reasons for the high correlation in 2010 were

similar: abundant oil supplies and fears about global growth. Interestingly,

around the second week of February 2010, the mood turned. The correlation

continued, but with oil and stocks both rising instead of falling.”

Given the large shorting activity around oil prices we could

see a short squeeze in oil that will benefit stock prices should the

relationship hold.

True U.S. oil production has leveled off and rig counts have

been dropping heavily. The question arises as to OPEC’s ability to adhere to

production cuts. Many experts don’t think so.

From Business

Insider, “Most recently, on Thursday,

The Wall Street Journal's OPEC correspondent Summer Said tweeted: "OPEC is

ready to cooperate on a cut, but current prices are already forcing non-opec

producers to at least cap output, says UAE Energy min."

But the Kingdom might

not be ready to fold just yet.

"Possible ongoing

talks on coordinated OPEC and non-OPEC crude oil production cuts are unlikely

to be successful in the near-term, in our view," argued BAML's MENA

economist, Jean-Michel Saliba, in a recent note to clients.

"Saudi Arabia

appears to be continuing in the meantime to position its energy and fiscal

policies for a lower for longer oil price environment, if need be, as suggested

by the possible flotation of Saudi Aramco or parts thereof."

And Saliba writes that

if the oil behemoth does go public, it "would be a landmark event."

"We believe that

a potential IPO of Saudi Aramco ... could assuage key macro concerns regarding

unsustainable debt accumulation and Fx reserves drawdown," he wrote.

"It also would confirm the economic reform credentials of the

current Saudi administration and its financial preparedness for a potentially

prolonged period of low prices, in our view."

Saliba also argues

that the conservative oil-price assumption in the Saudi's 2016 budget also

suggests that the Kingdom is "unlikely to capitulate on its energy policy

as the adjustment is being carried on the fiscal front."”

They go on to state, “Moreover,

he writes that it may not even be that compelling for the Saudis to cut in the

short/medium term (emphasis ours):

We have suggested

that, in the short-term, a unilateral cut from Saudi Arabia appears a

marginally revenue-positive move. This could

leave it indifferent between a unilateral cut and no cut, partly as other oil

producers would free-ride and encroach on Saudi’s market share.

This

"indifference" arises because a 1mn bpd cut would increase the fiscal

breakeven oil price by US$10/bbl and, concurrently, broad elasticity measures

would suggest a US$10-12/bbl move upwards in oil prices. However, the elevated

starting level for the fiscal breakeven oil price restricts such a policy,

given the budgetary flexibility required of a swing oil producer. In the medium-term, unilateral cuts would

likely be unambiguously revenue-negative as both the supply and demand curves

would respond to higher oil prices.”

“And, finally, another

interesting idea to consider is what the "signaling impact" of such a

coordinated cut could be — and how the Saudis may interpret this. "Headlines

on joint cut discussions have already managed to talk up oil prices.

Elasticities may likely be non-linear, suggesting a more marked impact on

prices from output cuts at low oil prices," he writes.

"This suggests

difficulty to control the extent of the oil price rebound, which could be used

by non-OPEC producers as a lifeline to initiate hedges or obtain additional

financing," he adds.

In any case,

ultimately, Saliba believes that the Saudis are "best placed" to sit

through the lower oil prices if there won't be coordinated policy action.”

We closed our short positions and booked profits for the

start of 2016. While we still believe the longer term trend for the market is

lower we understand that there will be reflex rallies on the way down. We

believe the market has washed out in the near term and lends itself to a rally

that could take the market higher for the remainder of 1Q16 and into 2Q16

before resuming its downward trajectory.

We cite “less negative” economic figures, excessive short

positions in stocks and oil, improving price action in the transportation

sector, excessive negativity in the S&P percent of bullish P&F

formation, bullish divergences on the daily SPX chart and oversold conditions

on the weekly SPX chart and oil stabilization.

We didn’t mention easing monetary policy as Mario Draghi

spoke this weekend with dovish comments and we expect the Fed to soften their

language over time as well.

Bottom Line: We are

going aggressively long here for the first time since November of last year. We

think there could be a powerful rally from these levels but continue to believe

the market lows for the year have not been set. We are looking for a strong

rally to end February and March. Come the second and third quarter of the year

we could see weakness again and we believe this is going to be the summer to

short the market. By the third and fourth quarter hopefully this downward trend

will bottom.

Joseph S. Kalinowski, CFA

Email: joe@squaredconcept.com

Twitter: @jskalinowski

Facebook: https://www.facebook.com/JoeKalinowskiCFA/

Blog: http://squaredconcept.blogspot.com/

Additional Reading

Weekly

Market Summary – The Fat Pitch

Weekly

Stock Market Outlook: Investor Pessimism Lingers – See It Market

Gold

And US Treasury Bonds Are At Price Extremes – See It Market

Have

Stocks Bottomed? These 2 Critical Indicators Reveal the Answer... – Daily Reckoning

S&P

500 Approaching Significant Levels - Dana Lyons' Tumblr

This is How

Financial Chaos Begins – Wolf Street

Oil

Glut Compounded By Cracks In Global Economy – OilPrice.com

$100

Trillion Up in Smoke – Mauldin Economics

No part of this report may be reproduced in any manner

without the expressed written permission of Squared Concept Partners, LLC. Any information presented in this report is

for informational purposes only. All

opinions expressed in this report are subject to change without notice. Squared Concept Partners, LLC is an

independent asset management and consulting company. These entities may have

had in the past or may have in the present or future long or short positions,

or own options on the companies discussed.

In some cases, these positions may have been established prior to the

writing of the particular report.

The above information should not be construed as a

solicitation to buy or sell the securities discussed herein. The publisher of this report cannot verify

the accuracy of this information. The

owners of Squared Concept Partners, LLC and its affiliated companies may also

be conducting trades based on the firm’s research ideas. They also may hold positions contrary to the

ideas presented in the research as market conditions may warrant.

This analysis should not be considered investment advice and

may not be suitable for the readers’ portfolio. This analysis has been written

without consideration to the readers’ risk and return profile nor has the

readers’ liquidity needs, time horizon, tax circumstances or unique preferences

been taken into account. Any purchase or sale activity in any securities or

other instrument should be based upon the readers’ own analysis and

conclusions. Past performance is not indicative of future results.

No comments:

Post a Comment