The market’s obsession with the inner workings of central

bank policy continues. The latest figures place the probability of a rate hike

at the end of this month at 0%. The probability is less than 30% for a hike in

June and July. It’s only until we reach the end of the year (December 2016) and

the start of next year (January 2017) that the probability of a hike exceeds

50%.

The Fed’s dual mandate of steady employment and prices

remain but has recently become a bit muddy as Chair Yellen has been basing

monetary policy decisions on unorthodox objectives. Year-over-year nonfarm

payrolls have been growing slightly above average over the past several years.

Inflation expectations have been quite low but have risen

recently. US Core PCE (seasonally adjusted) has started trending higher and

inflation expectation as measured by the risk premium between 10 year TIPS and

10 year government yields confirms the move. In fact, inflation expectations are

coming off the lowest levels since 2010.

The question remains what is keeping the Fed so dovish and

when will they have the confidence to start to take a more aggressive stance

towards tightening.

While the employment picture seems to be in-line with what

the Fed hopes to achieve and most likely price stabilization is running

slightly below target levels, the US and world economies continue to struggle

and perhaps the Fed lacks conviction of the US economy to withstand additional

tightening. While true the global stock markets have recovered from the furious

bout of volatility from earlier in the year, oil prices have staged a recovery

and China concerns have once again subsided, we are not out of the weeds just

yet. The International Monetary Fund just downgraded global economic growth

again citing concerns about strife in the Middle East, European refugee

concerns, the possibility of a British departure from the EU and anti-trade

sentiment that has stemmed from our political process. The rapid rise of the

Japanese Yen (we were bullish on the Yen in our March 7th blog

note) has splashed cold water on the Japanese economy in spite of moving to

negative interest rates.

First quarter economic growth for the US according to GDPNow,

the Atlanta Fed forecasting model that has been spot on recently shows the US

economy growing an anemic 0.3% in 1Q16. This is compared to just less than 1.5%

growth based on economist forecasts.

Indeed the economic analysis coming from the XE

Blog (they do a great job at tracking all things economic) states, “This week’s two primary releases were

coincident economic indicators that showed a slowing consumer and industrial

sector. Neither development is

encouraging as we begin the second quarter and both are likely culprits for the

Atlanta Fed’s GDPNow model’s decline to a .3% 1Q16 growth rate…With the LEIs

barely rising and much slower rate of growth for the CEIs, it’s doubtful we’ll

see stronger much growth in 2Q.”

Additional pressure on the global economic front comes from

the non-oil export figures out of Singapore. This country is considered to be a

good barometer for global growth as it has multiple trading partners in the Pacific

Rim. This morning Business

Insider reported, “As a global

barometer for the health of the global economy, Singapore continues to paint a

bleak picture at present.

Not only did its

economy fail to grow in the first three months of the year, demand for the

nation’s exports is now also plummeting.

According to

International Enterprise (IE), non-oil exports (NODX) from the country fell by

15.6% in the 12 months to March, missing already dire forecasts for a

contraction of 13.2%.

The annual contraction

was the steepest recorded since February 2013 and well below the 2.0% annual

gain previously recorded in February.”

“Although the data is

volatile, exports have now contracted on an annualised basis in three of the

past four months. As a major global trade hub, the continued weakness in

exports suggests global demand remains weak, underscoring concerns from the IMF

and others that global economic growth may once again undershoot expectations

in 2016.”

The economic picture in our view doesn’t warrant new highs

in the stock market and yet the market continues to climb. This leads us to

believe that the market is moving higher on the tenets of additional monetary

stimulus (or a departure from a tightening stance for the Fed) and a bout of

short covering. Take that with drastically reduced corporate earnings and

revenues and we have potential problems on the horizon. Not the greatest recipe

for a sustained market rally.

Other concerns that may hinder the Fed from further

tightening was brought to light from Deutsche Bank's chief US economist, Joe

LaVorgna (via Business

Insider). To summarize his points, here are the meeting dates and

additional reasons the Fed may stay its hand.

4/27/16 meeting – No rate increase due to slowing 1Q16

economic growth.

6/15/16 meeting – No rate increase due to sub-par 2Q16

economic growth and the volatility arising from the Brexit situation (that

meeting happens on June 23).

7/27/16 meeting – No rate hike because it coincides with the

Democratic National Convention (July 25-28) and is only a few days after the

Republican National Convention (July 18-21).

9/21/16 meeting – No hike due to the proximity of the US

general Presidential election.

11/2/16 meeting - No hike due to the proximity of the US

general Presidential election.

12/14/16 meeting – This would be the earliest the Fed could

hike if it were at all concerned about the above factors. It appears based on

the Fed implied probabilities that the market is expecting something similar to

the above scenario pending some obscure bout of growth or inflation.

Surprise Fed Action

If we toss fundamentals aside temporarily and assume the

market will be dictated by monetary policy, at least temporarily then a

surprisingly hawkish Fed statement or unanticipated move in rates could have

some fairly dire consequences. We believe the market has currently prices in an

increasingly dovish Fed which is expected given the state of the global

economic environment.

Investment Grade Bonds

On the daily chart, investment grade bonds have seen a

fairly parabolic move this year as the Fed softened its stance. The chart for

LQD (IG bond ETF) has had a strong move to the upside but we are starting to

see some negative bearish divergences between prices and the oscillators and

MACD. A hawkish Fed tone can bring this ETF lower. The LQD weekly chart looks

equally extended and is probably due for a pullback or at the very least a

consolidation period. The LQD monthly chart also shows several bearish

divergences as new highs in the index are met by lower highs in the technical

readings. Fed action counter to market expectations could mean trouble for the

sector.

High Yield Bonds

We are seeing bearish divergences all over the high yield

bond market. We are tracking this sector using the iShares High Yield ETF

(HYG). This sector has also seen big moves from its lows earlier in the year

and surprising central bank action will take its toll here as well. We are

concerned about these bearish divergences because high yield prices move very

closely with US stocks. The five year correlation coefficient between HYG and

SPX (S&P 500) is greater than 90%. More recently in the past twelve months

that relationship has come down to roughly 76% as prices between high yield

bonds and stock prices have diverged. We pointed out in previous writings that when

these divergences have occurred (stocks outperforming high yield bonds) it has

usually coincided with stock market corrections and in extreme cases bear

markets.

On a weekly basis, the high yield ETF is largely overbought

but remains in its downward channel. The recent parabolic rally came on lower

volume.

US Equities

On the daily chart the S&P 500 remains in its downward

channel despite the recent rally. The sugar rush from last week’s announcement of

an oil production freeze will be short lived in our opinion and isn’t a strong

enough catalysts to change our view. Economic growth and corporate earnings don’t

support current valuation levels in our view. The best chance we have of

continuing the rally to new highs will be excessively dovish Fed action. We are

seeing some potentially bearish divergences on the chart. Given the technical

picture as well as the earnings and economic fundamentals, we are still

expecting a rather rough and volatile summer market.

The weekly SPX chart shows an over-extended market that

still resides in a downward channel. The monthly chart has improved a bit but

far from ideal. Similar to the start of the last two bear markets, RSI (14) has

dipped below 50 but this time around it has retaken that level. That is a good sign. There has been

a MACD bearish cross, but that negative momentum has subsided somewhat. Prices

broke the 20-month moving average to the downside and the slope of the 20MMA

turned negative. We have recently retaken the 20-month average and it is

sloping higher again. If these metrics start to fail once again and the US

economic and corporate earnings picture doesn’t improve, we could see the

S&P 500 fall all the way to 1600 (which is the 38.2% Fibonacci level off

the 2009 bottom. Perhaps another round of QE or negative interest rate policy

by the Fed would save the day to avoid these levels

US Dollar

The US dollar has priced in the new dovish Fed. It has been

in a clear down channel recently but downside momentum has been waning. We

think it could drop back to the 93.5 level based on the daily chart. If this

level holds as support again it could offer another trading opportunity. On the

weekly chart the US dollar is oversold and approaching a key support level at around

93.5. If this level holds again it would offer a trading opportunity and if the

Fed makes an unexpected hawkish move, we could see the US dollar break the 100

level to the upside. The monthly chart shows positive momentum for the dollar

and would act as support for the coming trade near 93.5.

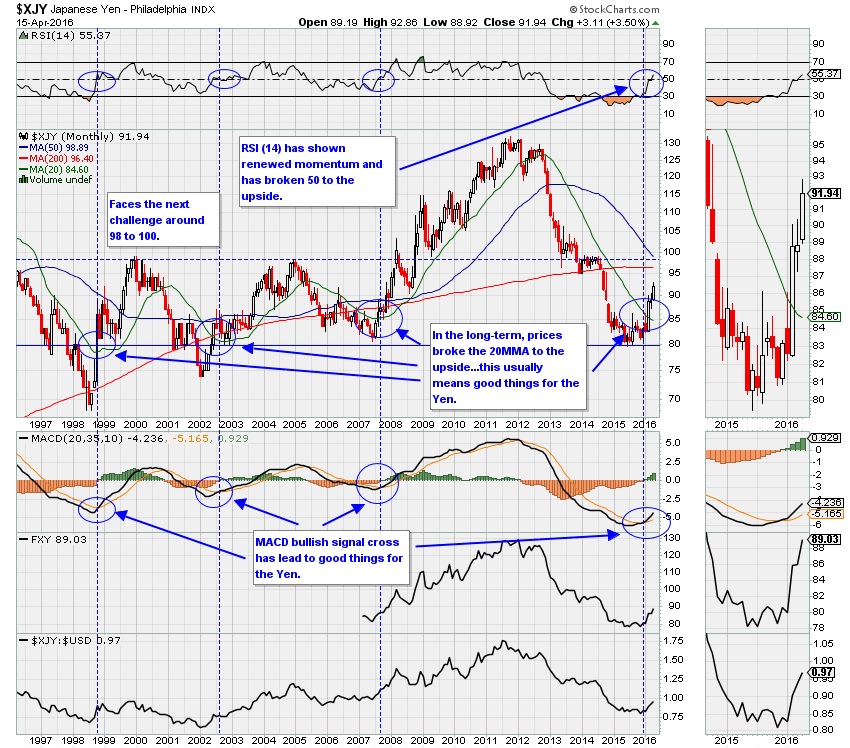

Japanese Yen

Clearly the rise in the Yen has frustrated Japanese policy

makers. Excessive quantitative easing and zero interest rate policies haven’t

stopped the Yen advance. This would most likely increase the chances of

additional Bank of Japan intervention although feedback from the recent G20

meeting indicates a lack of cooperation from other central banks and policy

makers. From Business

Insider, “Japan's efforts to seek

informal consent to act against an unwelcome yen rise bore little fruit, with

the United States offering a cool response to concerns voiced by Tokyo that the

currency's gains are too sharp and may justify intervention.

A lack of G20 sympathy

for Tokyo's appeal may embolden yen bulls to test the currency's 17-month highs

against the dollar hit earlier this month, keeping Japanese policymakers on

edge to contain the damage on a fragile, export-reliant economy… In a communique

issued on Friday, the G20 finance leaders maintained a warning on countries to

refrain from competitive currency devaluation and signaled that markets have

calmed from the past few months of turbulence.

The G20 also

reiterated that excess currency volatility was undesirable, but only after

heavy lobbying by Japanese delegates who want to use the language to justify

stepping into the market if they see yen gains as excessive.

Tokyo won't be

engaging in competitive currency devaluation as long as any yen-selling

intervention is brief and aimed at smoothing abrupt yen rises, a senior

Japanese finance ministry official told reporters after the G20 gatherings.”

They go on to cite, “the

government may lean on the Bank of Japan to deploy another blow of monetary

stimulus as early as its next rate review on April 27-28.

BOJ Governor Haruhiko

Kuroda waded into the currency debate to describe past yen rises as

"excessive," and reiterated his pledge to take additional monetary

easing steps if yen moves hurt the economy.

While many BOJ officials

are wary of acting again so soon after having deployed negative interest rates

in January, Kuroda may be ready to pull the trigger, some analysts say.

U.S. economist Nouriel

Roubini, who claims to have spoken to Japanese central bankers, signaled on

Friday the BOJ may be nervous enough about the yen's rise to ease even before

the April meeting.”

On the daily Yen chart, we are seeing some possible bearish

divergences off its most recent rally and a near-term pullback could be in

order. Momentum has been very strong on the weekly chart but we are approaching

levels that would coincide with government intervention, at least temporarily.

On the monthly chart we are seeing many bullish signs. RSI (14) has risen back

above 50 coincided with a bullish MACD cross. In previous instances this has occurred

prior to major upward moves in the currency and usually during periods of US

stock market turmoil. A long position in the Yen could provide cover if we get

a major stock market sell-off this summer. We could see a short-term pullback

but longer-term optimism.

The oil production freeze negotiations out of Doha this

weekend have broken down driving oil prices lower and providing a boost for the

Yen. From Bloomberg,

“The lack of agreement at Doha highlights

the deep divisions between OPEC members, and importantly, within Saudi Arabia,

said Robert Rennie, the global head of currency and commodity strategy at

Westpac Banking Corp. in Sydney. The Aussie should hold support from about

75.75 cents to 76 cents at least through the next day or so, he said.

The yen appreciated

0.3 percent to 108.41 per dollar. Earlier it touched 107.77, approaching the

107.63 level reached on April 11, the strongest since October 2014.”

The Yen remains a crowded long as reported by Bloomberg.

“Hedge funds and other large speculators

have never been more bullish on the yen.

Positions that benefit

from gains by Japan’s currency exceeded those that benefit from losses by a net

66,190 contracts in the week ended April 12, a report from the Commodity

Futures Trading Commission showed Friday. That’s the most in data going back to

1992.”

Gold

In the latest Commitment of Traders report for gold, we are

seeing a fairly crowded long speculative trade while commercial contracts show

the users of gold are locking in prices at current levels, an indication that

gold could head lower. From Seeking

Alpha, “In the latest Commitment of

Traders report (COT), we saw a week where speculative gold longs increased their

positions while speculative gold shorts slightly decreased their positions.

Speculative gold longs stand at over 200,000 contracts, which is the highest

since August of 2011 - when the gold price achieved its all-time high.

Additionally, commercial gold traders (bullion banks, producers, retailers,

etc.) increased their short position to the highest since February of 2013.”

“This week's report

shows a large increase in speculative longs with speculative shorts slightly

decreasing their positions.”

“As is clear in the

table above, speculative positioning significantly favors the long side as

speculative longs now hold 214,349 contracts versus the speculative shorts at

30,131 contracts.

This is the highest

nominal speculative long position since August of 2011!”

“The yellow line in

the table above is the all-time COT report high for the gold price at $1,895

per ounce. The big difference, though, is that currently we have around 30,000

speculative traders short gold, while in 2011, that was fewer than 5,000

contracts short - so even though we've hit nominal speculative long highs, the

percentage of shorts is still much higher now and that means there could be

room to grow.

Finally, when we take

a look at commercial traders (bullion banks, miners/producers, large merchants,

etc.), we see that they have significantly increased their short positions.”

“They have essentially

doubled their short positions into this gold rally, and their current short

position of over 194,000 contracts represents the biggest short position these

entities have held since February of 2013. Of course, when it comes to the COT

report there are always two sides to the trade as no short can be established

without a corresponding long and vice versa, but the fact that many of the

traders actually involved in the physical gold world are willing to take the

other side of the gold trade should at least make investors cautious.”

The daily gold chart (GLD) shows the big move for this year

and we appear to be in a consolidation phase. A trade may happen with a

breakout from the downward channel and selling pressure could on a breakdown

could be temporarily exacerbated by the crowded long. Momentum is clearly

improving but we’d be inclined to listen to what the commercial traders are

saying in their trading action.

On the weekly and monthly chart it seems we have snapped a

downtrend that has haunted the metal for some time.

Bottom Line

I’m not one to sell

in May and go away so I want to collect my thoughts on how this summer could

play out. It’s impossible to predict the future of capital market moves but we

are preparing for likely a direction based on specific events.

One key item will be

the Brexit vote in June. A vote in favor of a British exit from the EU could

cause some major summer volatility. If this occurs along with a decelerating

economic picture and a dovish Fed, we’d be inclined to be long gold, Yen and

treasuries and short US dollar, equities and high yield bonds.

If the economic

picture starts to improve heading into the second half of the year, the Fed

takes a more hawkish stance and the Brexit vote results in a no result for

exiting the EU we would take the opposite positions.

Joseph S. Kalinowski, CFA

Email: joe@squaredconcept.com

Twitter: @jskalinowski

Facebook: https://www.facebook.com/JoeKalinowskiCFA/

Blog: http://squaredconcept.blogspot.com/

Additional Reading

Gold

Could Be Heading Beyond $1,400 – Seeking Alpha

No part of

this report may be reproduced in any manner without the expressed written

permission of Squared Concept Partners, LLC.

Any information presented in this report is for informational purposes

only. All opinions expressed in this

report are subject to change without notice.

Squared Concept Partners, LLC is an independent asset management and

consulting company. These entities may have had in the past or may have in the

present or future long or short positions, or own options on the companies discussed. In some cases, these positions may have been

established prior to the writing of the particular report.

The above

information should not be construed as a solicitation to buy or sell the

securities discussed herein. The

publisher of this report cannot verify the accuracy of this information. The owners of Squared Concept Partners, LLC

and its affiliated companies may also be conducting trades based on the firm’s

research ideas. They also may hold

positions contrary to the ideas presented in the research as market conditions

may warrant.

This analysis

should not be considered investment advice and may not be suitable for the

readers’ portfolio. This analysis has been written without consideration to the

readers’ risk and return profile nor has the readers’ liquidity needs, time

horizon, tax circumstances or unique preferences been taken into account. Any

purchase or sale activity in any securities or other instrument should be based

upon the readers’ own analysis and conclusions. Past performance is not

indicative of future results.